I’m a cynic, so usually read industry reports published by industry providers with a huge pinch of salt, but every now and then you get an exception to the rule. So is the case with BigHand’s recently published ‘The Legal Pricing & Budgeting Report’, which is full of really insightful information (so read it!).

Here are my 10 take-outs (NA = North America and UK = UK):-

From

The damning:

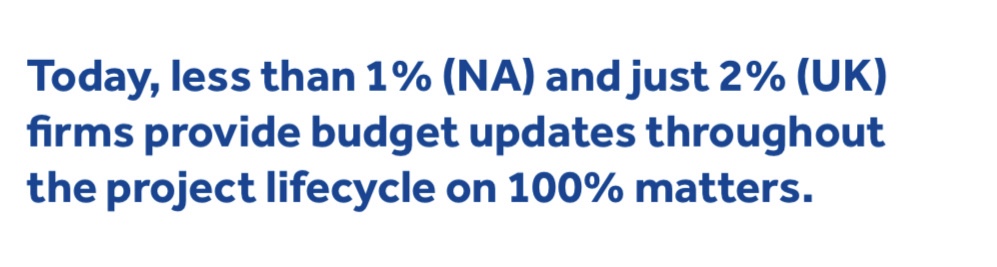

1.

To the surprising:

2.

3.

To some obvious:

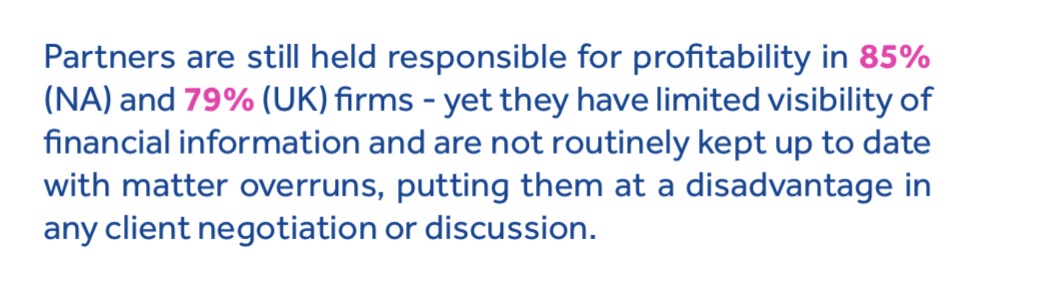

4.

5.

And some knowns:

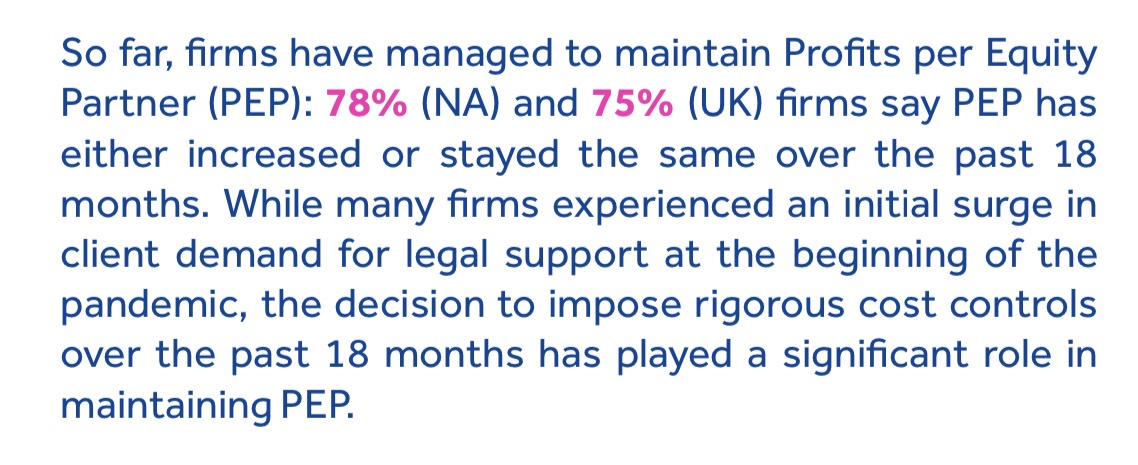

6.

7.

With a few, “What the?” (as in, only…)

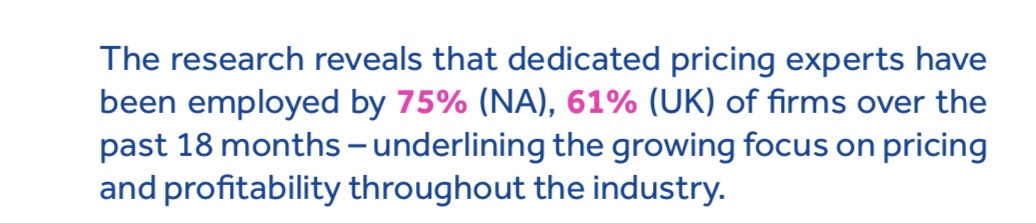

8.

9.

With a great conclusion:

10.

As I said, as a rule I don’t recommended reading these types of reports as they typically are a waste of time; but this is one I have no problem saying “go read it!” – and if you have any thoughts/comments, post them in the comments section below!

‘What would be some of the things I would want to be looking out for in a law firm’s invoice?

So here’s a quick list of my 10 things, but feel free to add your own 🤪 :-

Being charged [for]:

Expenses/disbursement – especially if they are unaccounted for (and particularly on fixed fee matters)

Travel time – especially if your lawyer is in the same town/city as you

‘Reading in’ time – especially when a new lawyer joins the team because one of the original team members has resigned or left the team

Team meetings to discuss your case/matter

Multiple lawyers attending the same meeting – especially if they have different time eateries

‘Out of scope’ work without a corresponding change order

Block billing of numerous tasks without explanation

Promotions – charge-out rates being increased for lawyers on your case because they have gain an additional year of post-qualified experience without adding any additional value

‘Bill padding’/‘Rounding up’ – when your lawyer rounds their time up to the next billable unit

‘Stickiness’ – where senior lawyers are doing work on your file that could be easily have been done by more junior lawyers, but they do it because they need to meet their internal billable targets.have different time.

As I say, feel free to add some of your own in the comments.

My friend John Chisholm hit the big time last week, he made the front-cover of Issue No.5 2021 of Legal Business World. All joking aside, John’s article ‘Who subscribes to your law firm?‘ (starts on page 8) is a really good read.

One of the gems I took away from John’s article is what he calls: ‘The 5Cs of Value’, which are (in his words):

Comprehend value to clients.

Create value for clients.

Communicate the value you create.

Convince clients they must pay for value.

Capture value with strategic pricing based on value, not costs and effort.

These are really good cornerstones to have, even if you don’t subscribe to John’s views of value-based pricing (did you see what an did there 🤪).

In any event, if you are new to the concepts of subscription and value based pricing, read the article because you’ll get a lot out of it.

And if you want to know more about the important topic of value based pricing in law firms, call him – but make sure to extract as much value as you can from him!

As far as I’m aware, Apple has never allowed retailers to discount (or have any other say in) its products pricing.

Ever.

As far as I have understood it, Apple’s rational for this because it has always insisted that it – and it alone – has complete control over its pricing.

Why is this important?

In short, because while you will see retailers heavily discounting every other computer software and hardware manufacturers’ products during this year’s EOFY (lockdown) sales, no such offer is made on Apple products.

You don’t see red ink on Apple product price tags.

Ever.

So what can law firms learn from this approach?

Always understand the value you provide to your clients

In short, as McNutt’s title suggests, Uber have introduced an ‘Upfront’ fixed fee pricing model option for its UK customers.

Wonderful news, and encouragingly McNutt writes:

“…with the introduction of upfront pricing, both the rider and the driver will know the exact cost of their trip before they confirm”.

As someone who enjoys knowing what I’m paying for upfront, this is nothing short of brilliant news (even though I don’t live in the UK nor use Uber 🙂 ).

But…

there’s only one small problem…

which is,

more often than not the rider actually doesn’t know upfront what they are paying for.

Why do I say that?

Well, because Uber UK’s ‘Upfront pricing’ offer comes with four [very small but somewhat important] scenarios under which the agreed Upfront price may change.

McNutt’s article sets these out as being:

If the rider adds or removes a stop in their journey;

If the final destination is more than one mile away from the originally requested destination;

If a detour is taken and the trip is further (40% and 0.5 miles further) and slower (20% and two minutes slower) than originally estimated; or

If the trip is at least 40% and 10 minutes slower in duration.

Let’s take a closer look at these:

If the rider adds or removes a stop in their journey – okay, on first read this one seems fair. But then I re-read this and saw ‘removes a stop‘; and asked myself: ‘How does removing a step make my fare more expensive (unless the change element here is to reduce the fare – which would be fair go!)?’

If the final destination is more than one mile away from the originally requested destination-again, seems fair. But it doesn’t say if this final destination is the ‘original’ final destination. If that is the case, why am I paying more for your miscalculation (see below)?

If a detour is taken and the trip is further (40% and 0.5 miles further) and slower (20% and two minutes slower) than originally estimated-not sure what a ‘detour’ is, but having been in the UK just before COVID I can tell you we did a lot of detours!

And so we come to bullet-point #4 – If the trip is at least 40% and 10 minutes slower in duration.

Here I have LOADS of issues.

As McNutt writes:

In other words, if you hit traffic and your trip has been extended by a significant amount of time, the fixed cost will likely increase.

Now that sounds a little wrong. A fixed cost that is allowed to increase because of a time-based element.

Taking a step back here, McNutt writes that:

Uber says that it bases the fixed price based on the best-available route between the rider’s pickup and dropoff points. It uses the expected duration and distance of the trip to come up with the exact figure, while taking into account anticipated traffic patterns and known road closures. Costs for tolls and additional surcharges will also be accounted for in the upfront pricing figure. When demand is high, Uber says it’ll account for that with “dynamic pricing” — a new take on surge pricing.

So Uber totally scopes the project, with information the rider likely doesn’t have access to (Google is good, but that good?), but then says: ‘If we got our calculation wrong, we get the right to readjust’.

To my mind this is essentially a ‘get of prison free’ card for Uber, which is fine – but let’s not then say this is Upfront fixed fee pricing, let’s call it out for what it actually is: a cost estimate at best.

And so why this post after so long away?

Well, no prizes for guessing what other (hint ‘professional services’) industry might have this type of fixed fee pricing mentality!!

As always, the above represent my own thoughts only and would love to hear yours.

In Episode 748 (7 July 2020) of HBR’s Ideacast podcast (23.04), Curt Nickisch interviews Rafi Mohammed, founder of the consulting firm ‘Culture of Profit’, on the topic of ‘Pricing Strategies for Uncertain Times‘.

During the course of the conversation Nickisch states that with COVID-19 service/product providers will be under intense pressure from clients/customers to offer discounts, to which Mohammed replies:

Clearly, in the short-run, you have to offer a discount. And what I would be focused on is what I call discounting with dignity in a manner that doesn’t devalue your product in the long run. And so, that’s really important because once you set a low price, it’s very hard to recover when demand eventually does come back.

And so we turn to how this really important concept applies to law firms

Blind Freddy can tell you that clients are under intense pressure to cut costs. I doubt there is a CFO out there who has not phoned (or even Zoomed) his/her GC and told them to cut costs.

And I suspect there are few GCs out there who have not responded by calling, zooming or even emailing the law firms on their legal panel to tell them to reduce rates by X%.

And, having lived through the Asian Financial Crisis of 1997 and the GFC of 2008, I suspect there are few law firms partners who have not passed along this request to their Finance Department with a note to “make it happen“.

But if this sounds familiar, and if a law partner you know would or has done this (*because it is never us*), then you would be missing out on Mohammed’s very powerful ‘discount with dignity‘ concept.

Because, as much a I hate advocating or agreeing to discounts, Mohammed is right:-

If you offer a discount to customers/clients merely because we are going through turbulent (or should I be saying ‘unprecedented’ 🙂 ) times, then what you are really doing is devaluing your service/product in the long term.

Because what you are saying to your customer/client when you unconditionally agree to a discount request of this kind is that “you have been over paying me all this time” – I’m not really worth what you have been paying me.

A Suggested Alternative Approach

Much like scoping in Legal Project Management methodology, when it comes to discounting (and I’m realistic enough to know that there needs to be some consideration of discounting in current times), you need to be considering what you take out of the basket when you offer that discount.

Which is to say it isn’t a ‘like for like’ for less conversation – you don’t get the same for less. If you take 15% off, you take 15% out of the basket. And you look to alternatives to how that can be sourced – either in-house or some other way (including LPOs/ALSPs).

And, if it really does need to be ‘like for like, but for less’ then it needs to come with a risk sharing collar. For example, I will accept 80% of my fees, but if we get past COVID-19 and your share price returns to pre-COVID highs within 6 months of completing this deal, then you agree to pay me 120% of my fees.

And, in the very worst of scenarios, your invoice should include a line item that states the discount being given is a one-off COVID-19 discount (and Mark Stiving, of Impact Pricing, has an interesting thought on this issue).

Regardless of what it is, you do need to do something. You cannot standstill for less. Because we will get past COVID. And in the ‘new world’ (even if that is a world where we merely live with COVID) there will be a ‘new, new normal’. And if you have agreed to discount your rates now without taking anything out of the basket, then what you have actually done is recalibrated your value in the new world.

And you won’t recover from that.

As always, the above just represent my own thoughts and would love to hear your thoughts.

When it first became apparent that COVID-19 was a pandemic – and one that we truly needed to be concerned about here in suburban Sydney, my doctor gave me a call. The call went something like this:

Doctor: “We need to make you ‘COVID ready’ Richard”.

Me: “Okay Doc, what’s COVID and how do we go about making me ‘COVID ready’?”.

We all now know what COVID is, and for a number of reasons – asthma, lack of general fitness and age group – I fell relatively squarely into what my doctor termed: the ‘vulnerable‘ (it sounded a lot less sinister then than it does now – now it’s actually a worrying tag).

His plan for preparing me to be ‘COVID ready’ (or at least better prepared) included walking 10,000 steps a day (and if you are wondering how far that is, it’s roughly 9kms). To help me (actually more importantly my doctor) track my success at achieving this daily task, I downloaded an app onto my iPhone and off I went.

Being the grumpy old man I am however, it didn’t take me long to come to the realisation that not every [walking] step is equal – a step walking up a steep hill takes a lot more effort than a step walking on a flat tarmac road.

But to the app they are the same. The app doesn’t distinguish between the effort of a step, it merely counts the number of steps!

So if you are still reading this – and you’re roughly 200 words in – you’re probably thinking:

“Fine, but what does this have to do with the business of law?”

And so here is my point – without trying to belittle the situation we are in at the moment:

If you are a lawyer and record your time by the billable unit, and have some kind of software to help you track that time, it won’t recognise the time and effort of the task you are undertaking: it will merely record the unit of time.

So much like my walking app records each ‘step’ I take, your billable software will record each [typically] six minute unit of time. It won’t give you any additional credit for the ‘effort’ (read difficulty) you put into that unit.

In fact, quite the contrary.

My walking app – and by extension my doctor monitoring it – gives me more credit for walking 15,000 steps a day on a flat and even surface than it does for walking 8,000 steps a day up a very steep inline that takes me three to four times more effort and for which I will ultimately be penalised by my doctor because I’m still 2,000 steps short of my daily target – despite the fact that overall I’m getting fitter, which is actually the ultimate goal!

So which of the two options do you think I go with?

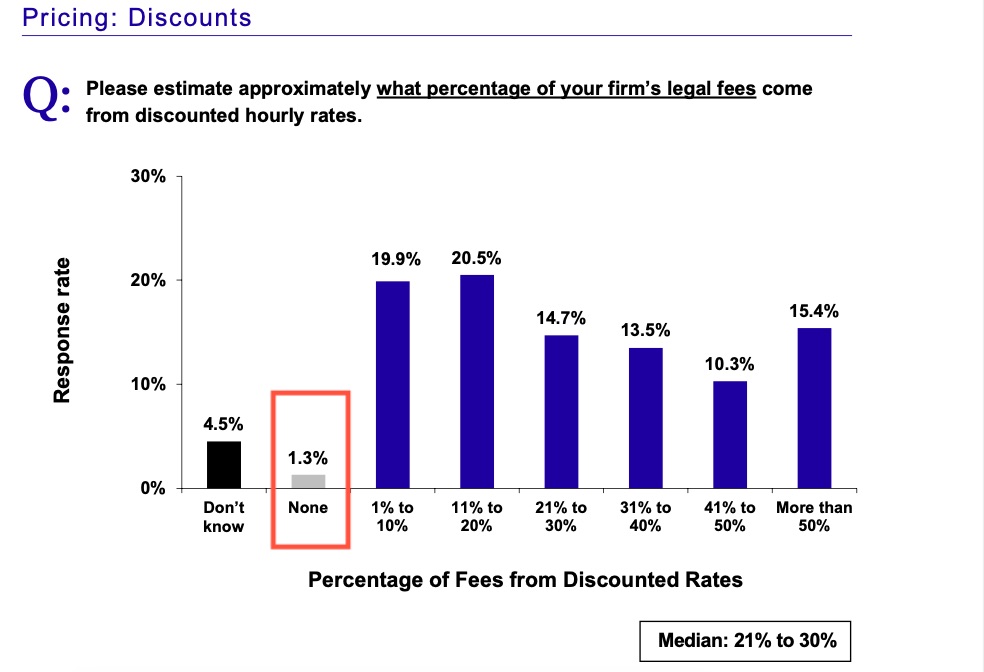

One of the most surprising take-outs from this year’s Altman Weil ‘Law Firms in Transition 2020‘ report is how little full freight fee collection is happening.

Keeping in mind that the collectable information in the report would have occurred pre-COVID, it is absolutely amazing to me that 98.7% of all hourly rates fees are now at “discounted hourly rates“.

To be fair, the term “discounted rates” is not defined and most law firms would argue – in this day and age – that they rarely get full freight rack-rate.

But it does make me wonder, if only 1.3% of your firm’s hourly rate legal fees are not discounted…

…why bother?

If becoming more progressive about how your firm prices is of interest to you then right now is the time to start thinking about this; because if all you are getting is 1.3% of your hourly rate fully realised…

…it’s time to start thinking outside the hourly rate pricing box!

As always, the above just represent my own thoughts and always interested to hear the views of others.

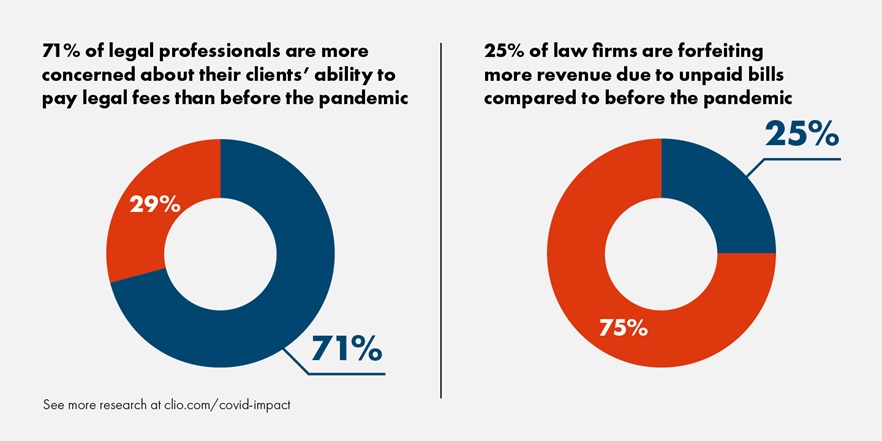

Having reported a cliff-fall in new matter instructions post-COVID in its Legal Trends ReportBriefing #1 in May of this year, June’s updated Briefing #2 by Clio shows a subsequent significant upward spike in new matter instructions that have, effectively, netted out year-on-year the number of new file matter instructions.

While, at first glance, a return to quasi-normal file opening matter numbers look to be good news for law firms, as the latest Briefing numbers also shows, if you scratch the surface you’ll soon see (diagram below) a far bigger underlying problem is starting to emerge – namely clients’ inability (or possibly unwillingness) to pay!

While the above wheel-chart is, at first glance, alarming, it’s also worth keeping in mind that a client’s ‘ability‘ to pay a legal fee pre and post the pandemic is not necessarily the same as its ‘willingness‘ to pay that fee. Which is to say there may be (and likely are) other underlying reasons as to why clients are saying they are not willing to pay fees – including a re-evaluation on the part of the client in respect of the perceived value being provided.

Of more concern to law firm management, however, should lie in the second of these two charts, namely the fact that rather than chasing fees 25% of firms are electing to forfeit the revenue.

Again, there could be a whole raft of underlying reasons why a firm may decide it would rather forfeit some of its billed revenue, and without undertaking a root-cause analysis we left to guess these (including my favourite – trying to preserve the relationship), but we should be left under no illusion that discounting and write-offs will have the biggest impact on profitability*.

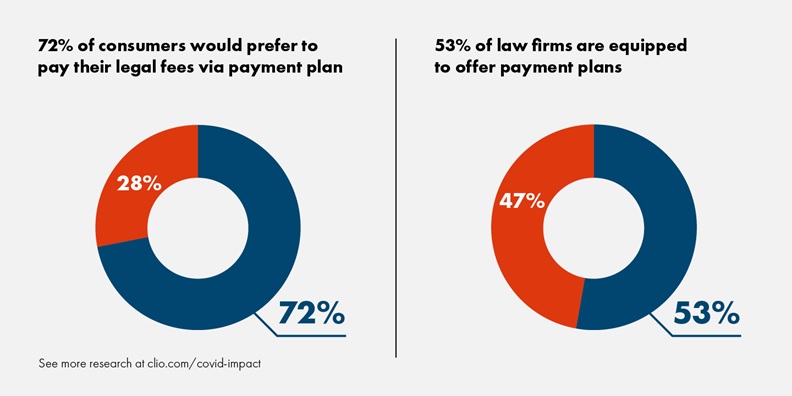

A willingness to look at alternative payment methods

For me, a somewhat surprising take-out from the latest Briefing was the statistic that 72% of consumers would prefer to pay their legal fees via a payment plan. Again, the term “consumer” isn’t defined and so we are left wondering if this is B2C or B2B; but even then, that only 53% of firms are equipped to offer payment plans seems odd.

Take away?

So what’s my top 3 take outs from this latest Briefing from Clio?

Once things settle down, law firms will be as busy as ever,

Cashflow will be king and clients are struggling with their own cash-flow, so

Think outside of the box when it comes to pricing and how you ask clients to pay and you should be okay.

As always, these just represent my thoughts and always interested to hear your views.

* N.B. If hourly billing is the way you work and you want to get a better understanding of the effect that discounting/write-offs has on your firm’s profitability, take a look at this post by Patrick Johansen that profiles Stuart Dodds’ ‘1-3-4 Rule‘