As far as I’m aware, Apple has never allowed retailers to discount (or have any other say in) its products pricing.

Ever.

As far as I have understood it, Apple’s rational for this because it has always insisted that it – and it alone – has complete control over its pricing.

Why is this important?

In short, because while you will see retailers heavily discounting every other computer software and hardware manufacturers’ products during this year’s EOFY (lockdown) sales, no such offer is made on Apple products.

You don’t see red ink on Apple product price tags.

Ever.

So what can law firms learn from this approach?

Always understand the value you provide to your clients

It’s something that has troubled me for a number of years:

Is the title of the job you do more important than the job you actually do?

For a long time I thought the whole debate was rather meaningless and irrelevant: do the job, be present, be a part of the team, kick goals.

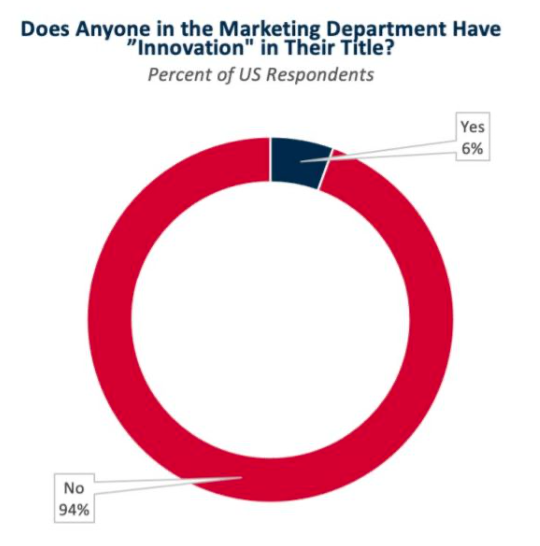

But last week I read a report by ALM Intelligence report that made me rethink this a little.

So, before I start, the ALM Intelligence report is an important study on equality of revenue (or lack there of) between the sexes in legal marketing. Nothing I write below should detract from that and we should all be horrified by the outcomes of the report.

Which then brings me to the point of this post – a totally unrelated graph in the ALM Intelligence report (I hope) on:

Which made me think again:

Is it the title or the job?

Because while I agree with the many in the discussion I had about this on LinkedIn: that it’s about the job, expertise and experience over the title…

I’m still left wondering…

…are Marketing and Business Development missing a trick here?

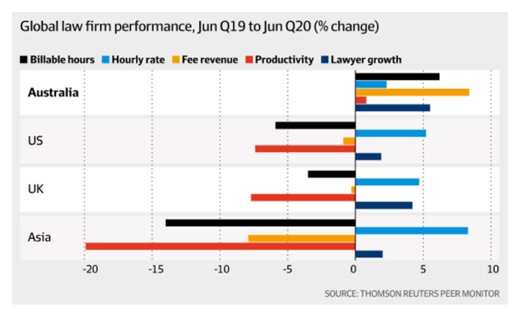

Citing a recently published Thomson-Reuters ‘State of the Legal Market 2020‘ report, The Australian Financial Review (AFR) published two articles last Friday (28 August 2020) that, collectively, provide one of the first insights in to how Australian law firms are fairing in this post-pandemic COVID-19 world.

How is Australia doing compared to the rest of the world?

The first article ‘Law firms prove world-beaters as virus strikes‘ by Michael Pelly would, at first blush, seem to suggest that law firms here in Oz are doing far better than the rest of the world.

Looking at the five key metrics of:

billable hours,

hourly rates,

fee revenue,

productivity, and

lawyer growth,

Australia’s results look spectacular.

But kick the tires a little and you’ll see that a June Q19 to June Q20 period is an Australian Financial Year – and not all, in fact none of the other regions, works to that same time line.

So these results should be read with caution, in that they are a moment in time which may not be a true reflection of how the other markets are fairing (it would be interesting to run those same numbers on a Jan to Dec timeline which would probably be a truer period [admitting that even then the UK numbers would be out] because, as we know, not every month is equal – in that we don’t split an annual budget by 12!).

Nevertheless a good result for the Oz firms – but that ‘red blip’ of productivity would be a concern to me if I were a Managing Partner.

Which leads us to…

…who is doing the work?

One of the more interesting takeaways from the chart above is how the hourly rate in every geographic region has increased, even where fee revenue and number of billable hours has decreased (and in some cases significantly).

For those who may not have read my post of two weeks ago there are, in my view, two reasons why you get that kind of spike:- (1) the work is more complex and needs more grey-haired thought, or (2) senior lawyers need to protect their budget – your choice.

So where are we at really?

I’d treat the financial results of the Australian law firms above with a pinch of salt till the end of February 2021, which -in my opinion – will be a truer barometer of how the industry is doing down here.

As always, the above just represent my own thoughts and would love to hear your thoughts (and; ps: if you want to know why I say end of Feb 2021, email me).

The Law of Supply and Demand The law of supply and demand is a theory that explains the interaction between the sellers of a resource and the buyers for that resource. The theory defines what effect the relationship between the availability of a particular product and the desire (or demand) for that product has on its price. Generally, low supply and high demand increase price and vice versa.

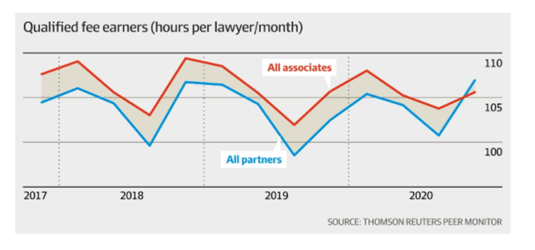

Results published in Peer Monitor’s Q2 2020 Report last week suggest that the broader economy has a lot to learn from running a law firm.

Why would I say this?

Well, what would you think would be the logical outcome from:

Average demand for legal services decreasing by 5.9%, and

Productivity across all fee earners declining by 7.2%?

In normal circumstances you would be given credit for thinking that prices would come down, or at least hold firm. But as we know, running a law firm is anything but normal circumstances because as the Report goes on to state:

Average worked rate charged across the market was 5.2% higher than at the same point last year.

That’s worth repeating: Higher! 5.2% Higher!

If you are wondering how that can even be possible, the answer is relatively simple: ‘partners [of law firms] have begun completing a higher proportion of [the] work by volume.‘

I would be the first to admit that one possible reason why this [partners doing more of the work in a leverage model – see my post here on leverage] can be the case is because the type of work being done by law firms has become far more complex since the onset of COVID-19 and this requires more grey-haired advice with a higher proportion of leverage at partner level. After all, none of us have lived through a pandemic of this nature and so there really isn’t much precedent for young lawyers to go looking for and so partners and senior lawyers are needing to be more hands on when it comes to file time.

But the cynic in me also thinks that’s a likely to be load of rubbish. Law firms (like many in the economy I will add) have been furloughing staff and making staff redundant during the pandemic. On the flip-side, budgeted number of billable hours for individual lawyers do not appear to have been reduced (other than pro-rata to the number of days lawyers may need to be taking off).

And so we find ourselves in this position where individual billable hour targets still need to be met, but overall demand for legal services is falling.

So what happens when this happens?

If we learnt anything from the data of Great Recession it is this:

In times of signifiant economic downturn, holding individuals to individual budgets results in an upstreaming of work.

Partners will hoard work in an attempt met their budget first

Special Counsel will hoard work in an attempt to met their budget second

Senior Associates will hoard work in an attempt to met their budget third.

And if you are outside of the gold, silver or bronze medal positions you’re pretty stuffed!

So what can we do about this?

For those sitting around wondering what can be doe about this, the answer is appears to be pretty clear – do away with individual utlisation and budgetary targets. Even in the best of years these so-called budgets are arbitrary in determining law firm profitability (primarily because they work on an opportunity cost profit basis rather than a real in the bank profit analysis), but more importantly because they create silos – individuals in law firms with personal incentives that outweighs those of the group/society.

And, they sustain bad behaviour in firms – ‘me’ over ‘us’.

But critically, firms that work like this create ‘Motels for Lawyers’ – not law firms.

As always, the above just represent my own thoughts and would love to hear your thoughts.

When it first became apparent that COVID-19 was a pandemic – and one that we truly needed to be concerned about here in suburban Sydney, my doctor gave me a call. The call went something like this:

Doctor: “We need to make you ‘COVID ready’ Richard”.

Me: “Okay Doc, what’s COVID and how do we go about making me ‘COVID ready’?”.

We all now know what COVID is, and for a number of reasons – asthma, lack of general fitness and age group – I fell relatively squarely into what my doctor termed: the ‘vulnerable‘ (it sounded a lot less sinister then than it does now – now it’s actually a worrying tag).

His plan for preparing me to be ‘COVID ready’ (or at least better prepared) included walking 10,000 steps a day (and if you are wondering how far that is, it’s roughly 9kms). To help me (actually more importantly my doctor) track my success at achieving this daily task, I downloaded an app onto my iPhone and off I went.

Being the grumpy old man I am however, it didn’t take me long to come to the realisation that not every [walking] step is equal – a step walking up a steep hill takes a lot more effort than a step walking on a flat tarmac road.

But to the app they are the same. The app doesn’t distinguish between the effort of a step, it merely counts the number of steps!

So if you are still reading this – and you’re roughly 200 words in – you’re probably thinking:

“Fine, but what does this have to do with the business of law?”

And so here is my point – without trying to belittle the situation we are in at the moment:

If you are a lawyer and record your time by the billable unit, and have some kind of software to help you track that time, it won’t recognise the time and effort of the task you are undertaking: it will merely record the unit of time.

So much like my walking app records each ‘step’ I take, your billable software will record each [typically] six minute unit of time. It won’t give you any additional credit for the ‘effort’ (read difficulty) you put into that unit.

In fact, quite the contrary.

My walking app – and by extension my doctor monitoring it – gives me more credit for walking 15,000 steps a day on a flat and even surface than it does for walking 8,000 steps a day up a very steep inline that takes me three to four times more effort and for which I will ultimately be penalised by my doctor because I’m still 2,000 steps short of my daily target – despite the fact that overall I’m getting fitter, which is actually the ultimate goal!

So which of the two options do you think I go with?

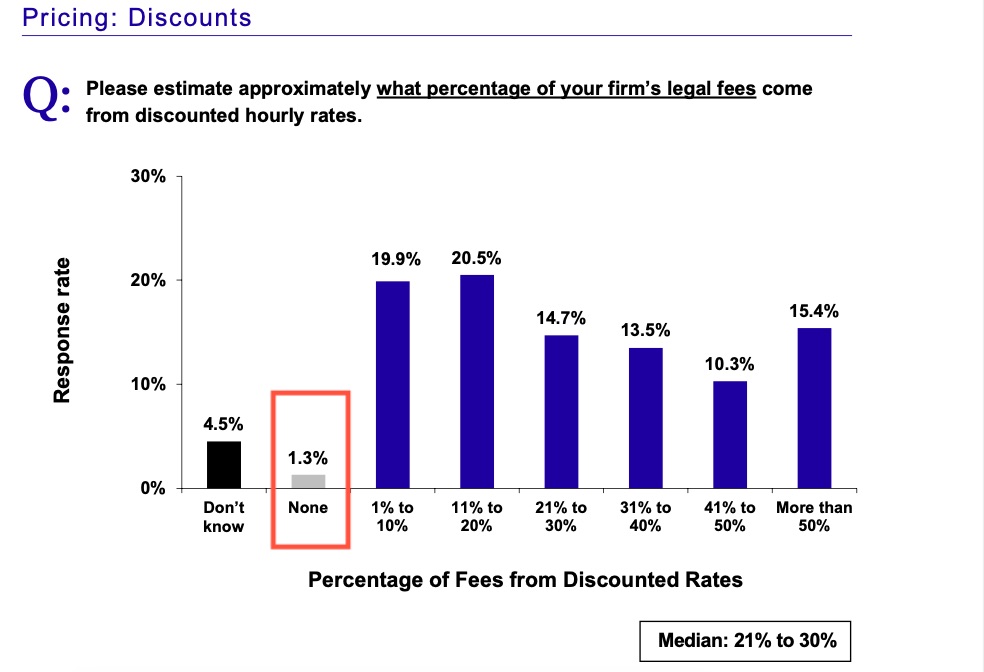

One of the most surprising take-outs from this year’s Altman Weil ‘Law Firms in Transition 2020‘ report is how little full freight fee collection is happening.

Keeping in mind that the collectable information in the report would have occurred pre-COVID, it is absolutely amazing to me that 98.7% of all hourly rates fees are now at “discounted hourly rates“.

To be fair, the term “discounted rates” is not defined and most law firms would argue – in this day and age – that they rarely get full freight rack-rate.

But it does make me wonder, if only 1.3% of your firm’s hourly rate legal fees are not discounted…

…why bother?

If becoming more progressive about how your firm prices is of interest to you then right now is the time to start thinking about this; because if all you are getting is 1.3% of your hourly rate fully realised…

…it’s time to start thinking outside the hourly rate pricing box!

As always, the above just represent my own thoughts and always interested to hear the views of others.

As we approach end of Financial Year here in Australia many will be looking at finalising, and implementing, their strategic plans for FY2021.

With this in mind I thought I would share my own base-level planning tool; my go-to starting point for any short, medium and long-term planning activity – I call it my ‘5 x 5 Planning Tool‘, it has served me well and works like this:

5 Minutes: Will the decision I make have an affect/effect 5 minutes from now?

5 Days: Will the decision I make have an affect/effect 5 days from now?

5 Weeks: Will the decision I make have an affect/effect 5 weeks from now?

5 Months: Will the decision I make have an affect/effect 5 months from now?

5 Years: Will the decision I make have an affect/effect 5 years from now?

It’s rare, but possible, that a decision you make will have an affect/effect on all five plains; but, in my experience, what the above does do is give you clarity. It allows you to compartmentalise thoughts into the short, medium and long-term and gives you the ability to then focus on what is then, in that moment, important to you and your business.

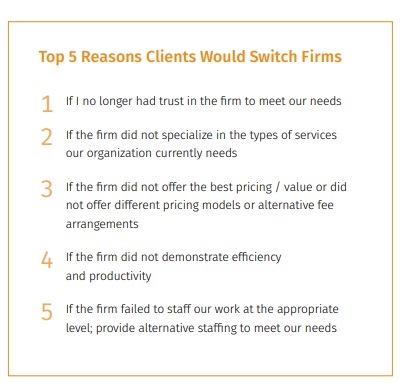

If you’ve recently lost a client to a competitor and have been wondering how that happened, wonder no longer. The recently published ‘2020 Future Ready Lawyer Survey: Performance Drivers‘ by Wolters Kluner has the answer.

Surveying 700 in-house and private practice lawyers across the US and EU in January 2020, this is probably the most comprehensive survey post COVID (although most of us were not entirely sure what this meant in January so I look forward to a survey report that has been conducted post March this year).

The Top 5 reasons cited as to why a client might leave your firm are:

The client no longer trusts your firm can meet their needs,

Your firm doesn’t specialise in the area of law needed by the client,

Your firm failed to communicate its value proposition properly,

Your firm did not demonstrate efficiency and productivity, and

Your firm’s leverage was/is all wrong.

And three of these are essentially because you messed up on sourcing, communicating and delivering on your pricing promise.

Take-away top tip: want to make sure you keep clients and keep them happy – make sure you (and your team):

understand(s) your value proposition and are able to communicate this,

get your team’s leverage right [hint: don’t hoard work at the top end just so you can meet budget this year!], and

understand the scope of what you are being asked to do and project manage both the scope and the client expectations (especially if out of scope creep occurs).

Manage this well, and you’ll be three-fifths of the way to keeping your client happy!

Demonstrate Efficiency

As a bonus, think about how you demonstrate efficiency to your client.

Is this by saying you have the relevant expertise/experience so that you can do this faster than others,

Is this by saying you have the appropriate IT systems that allow you to get the job done faster, or

Does efficiency even really matter – should the conversation not be about being an effective lawyer?

As always, these just represent my thoughts and always interested to hear your views.

The goal isn’t to find people who have already decided that they urgently want to go where you are going. The goal is to find a community of people that desire to be in sync and who have a bias in favor of the action you want them to take.

In around 2009 I recall reading Seth Godin’s, then recently published, blockbuster ‘Tribes: We Need You to Lead Us‘ and thinking this would have a profound impact on the way clients engage law firms. To give this thought some context, it was around the same time as we had started talking about a new fad called ‘unbundled legal services‘ (which would later also become known as ‘limited scope representation‘ – see ‘The great unbundling of legal work‘ in the Australian Financial Review). It was also a time when ‘disaggregation‘ and the rise of Legal Process Outsourcing (LPOs) (predominately in India at that time but later this would extend to South East Asia and South Asia) would have many of us who worked on bids and tenders discussing issues around disruption of the legal services supply chain – if for no other reason than clients were asking us to provide answers to these questions in their requests for tenders.

A cold wind, amounting to real structural change, in the way clients purchased their legal services was coming (Pfizer Legal Alliance).

THE ‘NEW NORMAL 1.0’

Fast forward a decade and probably the only person who still talks to me about Seth’s Tribes is my good friend Julian Summerhayes, and it is never within the context of an RFT or legal services more broadly.

Nope, in short tribes, disaggregation and unbundling, while definitely remaining vogue, never really had the impact and penetration that I – and I would suggest many others – thought they would.

The ‘New Normal 1.0’ had, to all practical purposes, failed.

KRYPTONITE TO THE ‘NEW NORMAL’ – TEAMS

Probably the biggest obstacle to the growth of tribes post 2009 has been the role that teams have historically played within the legal profession.

Since the times of Dickens a junior apprentice lawyer has worked with, and been mentored by, their senior (supervising) partner. It has always been thus, and with it has come an almost umbilical cord tie between lawyers who have worked in the same team.

Many an in-house General Counsel has sat at the foot of the table of the private practice partner to whom they send instructions. A relationship that has been forged within the confines of a team structure.

TRIBES REBOOTED – TRIBES 2.0

It’s my opinion that one of the biggest likely outcomes COVID-19 will have on the profession is the re-emergence of tribes – tribes 2.0!

There are a number of reasons why I think this might be the case, but probably the biggest is that in-house counsel have, over the past three months, become used to working with remote teams.

It should not, then, be too far removed to say that in-house counsel will be happy working with subject matter experts across firms who can enable them to achieve their objectives rather than with an individual firm that might get them across the line.

In short, on the right deal, in-house counsel will be happy to work with a group of lawyers from various law firms rather than one firm – a tribe over a team.

THE CHALLENGES

Moving from teams to tribes is not a foregone conclusion, it faces challenges.

High among these will be:

How is risk allocated?

Who wears the professional indemnity risk?

My own view is that these can be overcome with:

properly scoped Engagement Letters

proper use of Legal Project Management

a good understanding of Workflow Process Methodology

But that still leaves the issue: How do we price the ‘New Normal 2.0’?

HOW TO PRICE THE ‘NEW NORMAL 2.0’?

The cynic in me says that many law firms will not have the first idea how to price the New Normal 2.0. This presents a significant problem because if they cannot price it, then they cannot sell it (pricing still remains the principal form of credentialisation despite, or rather because of, whatever experience you claim to have).

ONE ANSWER – THE ROLE OF SCOPE PRICING IN THE ‘NEW NORMAL 2.0’

Scope pricing will play a critical role in the pricing in the ‘New Normal 2.0’.

Unlike a fixed fee, capped or fee estimate pricing, scope pricing does it exactly what it says on the tin – it prices to the scope of work being undertaken by the relevant lawyer. This means that proper use of scope pricing should allow in-house to teams to unbundle the legal work within their project – either between the role the in-house plays and the role the private practice firm plays; or, in the case of this post, the role that multiple lawyers with subject matter expertise from various firms play in a project.

And, if done properly, the biggest upside to scope pricing over any other type of pricing of legal services is that, by definition, there really shouldn’t be any scope creep – what you see [in the tin] is what you get!