The most recent Wells Fargo report on the state of the US market has just been published. While obviously US centric, I’m sure many of the trends are being reflected elsewhere, so worth a look.

𝗦𝘁𝗿𝗼𝗻𝗴 𝗶𝗻𝗱𝘂𝘀𝘁𝗿𝘆 𝗽𝗲𝗿𝗳𝗼𝗿𝗺𝗮𝗻𝗰𝗲 𝗱𝗲𝘀𝗽𝗶𝘁𝗲 𝘂𝗻𝗰𝗲𝗿𝘁𝗮𝗶𝗻𝘁𝘆

Global economic and geopolitical volatility has not slowed Big Law growth (so far)

Rates increased ~𝟭𝟭–𝟭𝟮%, the primary contributor to revenue growth

So far, minimal client pushback despite sustained increases

𝗖𝗼𝗹𝗹𝗲𝗰𝘁𝗶𝗼𝗻𝘀 𝗮𝗻𝗱 𝗰𝗮𝘀𝗵 𝗳𝗹𝗼𝘄 𝗲𝗺𝗲𝗿𝗴𝗶𝗻𝗴 𝗮𝘀 𝗮 𝗿𝗶𝘀𝗸

Collection cycle have slowed (~6.5 days longer)

Inventory (unbilled/uncleared work) is rising faster than revenue

End-of-year performance will depend on converting work to cash

𝗢𝗽𝗲𝗿𝗮𝘁𝗶𝗼𝗻𝗮𝗹 𝘁𝗿𝗲𝗻𝗱𝘀

Productivity is up modestly (+1.2%)

Headcount growth is steady (~3.3%)

Expenses are rising (especially in senior staff and technology)

𝗠𝘆 𝘁𝗵𝗿𝗲𝗲 𝘁𝗮𝗸𝗲𝗮𝘄𝗮𝘆𝘀

𝟭. The impact AI is having on demand is still minimal (actually, it is increasing work on the demand side!). On the productivity side, this may change, but increase demand is, so far, taking up any excess capacity. This (as well as the other indicators in the report) most likely means the Billable Hour will still be with us for some time to come.

𝟮. Realisation rates and increased collections times should be a real concern. No point charging $1,000 an hour if you never get paid!

𝟯. Amen to this!! – many firms have figured that rates are part of their branding, “and it’s very short-term thinking to try and manipulate rates downward to offset a decrease in demand.”

My thanks to the team at Legal Practice Intelligence for publishing my thoughts on whether or nor Australian law firms have given up on their Asia dreams following the recent decoupling of King & Wood and Mallesons.

If you want to read the article, here is the link.

The most recent – 2026 – Citi Hilderbrandt Client Advisory Survey Report published earlier this month contains some interesting commentary on how US law firms faired in 2025. None more so than the finding that:

a growing number of firms estimating that more than half their revenue will come from pre-negotiated discounts. (page 23)

Pre-negotiated discounts

The Report does not explicitly define “pre-negotiated discounts”; however it refers to alternative fee arrangements (AFAs) as including fixed, capped or blended rates. It is, therefore, reasonable to interpret “pre-negotiated discounts” as encompassing agreed reductions to standard charge-out rates, volume-based discounts and other upfront pricing concessions.

Viewed positively, this trend signals a shift away from reactive, end-of-matter discounting towards earlier and more deliberate pricing discussions. In principle, this should create a stronger foundation for meaningful conversations about value-based pricing, particularly where clients are seeking price certainty, predictability and risk sharing. From that perspective, pre-negotiated pricing is not inherently problematic — and may in fact represent a necessary transitional step.

The more concerning implication, however, is that for many firms these discussions appear to be anchored primarily in discounting, rather than in value definition. Where pricing conversations begin and end with rate reductions, firms risk reinforcing a price-taker mindset rather than asserting their role as price-setters. Left unchallenged, this dynamic contributes to margin erosion, commoditisation of legal services and an imbalance in client-firm relationships that becomes increasingly difficult to unwind.

AFAs as a pricing option

Despite persistent commentary throughout 2025 that artificial intelligence (ai) will fundamentally disrupt — or even eliminate — the billable hour, the data in this Report suggests otherwise. The proportion of revenue derived from AFAs has remained effectively flat, increasing only marginally from 23.5% in 2024 to a projected 23.6% in 2025.

Setting aside the fact that many commonly cited AFAs are, in reality, variations of the billable hour by another name, and acknowledging that it may still be too early to fully assess AI’s structural impact on pricing legal services, one conclusion is unavoidable: the billable hour remains very much alive.

The way forward

With 74% of firms expecting a growing proportion of revenue to come from AFAs by 2027, the issue is not whether pricing models will continue to evolve, but how deliberately firms choose to engage with that evolution; and whether AFAs are used as strategic tools or simply as discounted billing mechanisms.

In sum

Taken together, the findings in this Report further highlight a profession at an inflection point. While the billable hour continues to dominate, the steady rise of pre-negotiated discounts and the anticipated growth in AFAs suggest mounting client pressure for greater certainty, transparency and perceived value.

The critical question for law firms now is not whether they should offer alternative pricing arrangements, that horse has bolted, but whether they are prepared to move beyond discount-led negotiations and engage in genuine upfront value-based pricing conversations.

Firms that continue to compete primarily on price risk entrenching themselves as price-takers in an increasingly sophisticated procurement environment. Those that invest in articulating value, pricing outcomes and structuring risk intelligently will be far better positioned to protect margins and strengthen client relationships in the years ahead.

The decision on the way forward now rests with the firms themselves.

The size of your firm has no bearing on the amount you can charge clients.

Now if you have read the above quote and thought to yourself “of course the size of your firm has no bearing on the amount you can charge clients, clearly Smith has lost it again!“, then bear with me.

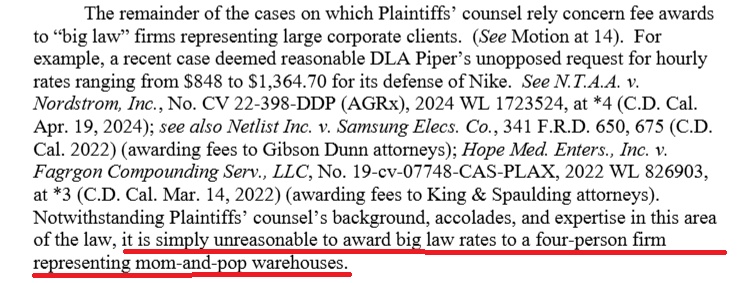

In a recent matter before the Central District of California, the Honorable Michael W Fitzgerald disagreed with the notion that the size of a law firm should have no bearing on the amount you can charge clients when he stated:

“it is simply unreasonable to award big law rates to a four-person firm representing mom-and-pop warehouses.”

In what is otherwise far reaching commentary on the history and application of the billable hour (well worth a read in itself), Fitzgerald’s ruling is troubling; not least because it is based on a premise that bigger means better — and better means more expensive. Now that could be true. But it doesn’t make it so.

Conversely, should I, as a client, be happy to pay more because the attorney acting on my matter works in a firm that has seven floors over one that has one? Surely the answer here is “no”, I’m paying for outcomes over inputs.

But that’s not the case here. If we follow Fitzgerald’s reasoning in this case, the real drivers of price: (a) Perceived expertise and relevance; (b) Client experience and accessibility; and (c) Outcome certainty and risk management, are certainly consideration, but no longer primary.

Read pretty much any report on the legal market over the past 20 years and the story is the same: Growth, growth, growth. But, a recent report by legal advisory boutique Taha & Watmough would suggest that, while that may be true at some level, the real story is a little less rosy.

Nearly all top [UK] 100 firms have seen real-terms rises in revenue and profit over the past ten years;

60% of firms have seen their revenue per lawyer fall in real terms;

60% of firms have seen profit per lawyer shrink;

More than a third of firms have seen partner profits decline.

Meaning the average equity partner at a top 100 [UK] law firm is earning less [in real terms] today than 10 years ago.

Given the rise in salaries and other costs here in Australia over that period, I wouldn’t see our numbers as being too different to those above.

So the next time you see stats telling you how well law firms are doing, remember:

“Vanity metrics are the fine China of analytics – pretty to look at, but useless at the table.”

Get in touch if you want to have a chat about how you can sustainably grow your firm

Private equity has scored a partial victory in its push to expand in the US legal market, after lobbyists softened legislation in California that threatened to disrupt liberalisation of law firm ownership rules. Attorneys in the country’s largest state will be allowed to partner on some legal work with investor-owned law firms under the terms of a law signed by Governor Gavin Newsom.

What Does This Means for the US Legal Market?

By far the largest legal market in the world, what does this development mean for the future of the US – indeed Global – legal market? While this compromise isn’t a full liberalisation of the Californian (let alone US) legal market, along with the recent liberalisation of neighbouring Arizona’s legal market, which now allows non-lawyers to own law firms under an “alternative business structure” (ABS) model, it’s certainly a crack in the door. For private equity, it’ll be a sign that resistance to change from within the profession can be negotiated down. For California’s legal establishment, it’s a signal that – finally – the status quo is no longer politically or economically inevitable. For the Global legal market, it’s further evidence, if it were needed, that despite all of the challenges that come with owning a law firm, private equity very much remains interested in this asset class.

Earlier today The 𝘈𝘶𝘴𝘵𝘳𝘢𝘭𝘪𝘢𝘯 𝘍𝘪𝘯𝘢𝘯𝘤𝘪𝘢𝘭 𝘙𝘦𝘷𝘪𝘦𝘸 published the results of its Law Graduate Salary Range Survey.

Makes for an interesting read. On the one hand, nowhere near as high as overseas markets such as London, HK and the US. On the other hand, Grads on A$130K would have been unthinkable 5 – 10 years ago!

𝗛𝗼𝘄 𝗺𝘂𝗰𝗵 𝗶𝘀 𝗮 𝗵𝗮𝗻𝗱𝗯𝗮𝗴 𝘄𝗼𝗿𝘁𝗵? In this case, a staggering A$15.3 million.

𝗧𝗵𝗲 𝘃𝗮𝗹𝘂𝗲 𝗼𝗳 𝘀𝘁𝗼𝗿𝘆𝘁𝗲𝗹𝗹𝗶𝗻𝗴 Unlike most handbags however, this one has a story to tell.

It was the very first Birkin bag.

Designed by Hermès executive Jean-Louis Dumas in 1984, following a chance encounter on a flight with actress and singer Jane Birkin (hence the name), the bag was used daily by Birkin for nearly a decade before she donated it to an Aids Charity auction.

What the sale of this bag evidences though is how value extends beyond material worth. Value is not the $$$ signs you seen on the price-tag; it’s about the stories we tell, the history we preserve, and the emotional connections we forge.

The sale of this bag is a powerful reminder to professionals that authenticity and narrative can elevate your service offering from ordinary to iconic.

It is your powerful – and likely only – differentiator. It is what clients are willing to pay for.