Read pretty much any report on the legal market over the past 20 years and the story is the same: Growth, growth, growth. But, a recent report by legal advisory boutique Taha & Watmough would suggest that, while that may be true at some level, the real story is a little less rosy.

Nearly all top [UK] 100 firms have seen real-terms rises in revenue and profit over the past ten years;

60% of firms have seen their revenue per lawyer fall in real terms;

60% of firms have seen profit per lawyer shrink;

More than a third of firms have seen partner profits decline.

Meaning the average equity partner at a top 100 [UK] law firm is earning less [in real terms] today than 10 years ago.

Given the rise in salaries and other costs here in Australia over that period, I wouldn’t see our numbers as being too different to those above.

So the next time you see stats telling you how well law firms are doing, remember:

“Vanity metrics are the fine China of analytics – pretty to look at, but useless at the table.”

Get in touch if you want to have a chat about how you can sustainably grow your firm

I put a post up last week on LinkedIn, off the back of a very interesting blog by Jordan Furlong on his Substack feed: ‘The legal world in 10 years (if we’re really lucky)‘, that got some social media traction so I thought I would re-share here.

At the heart of my LinkedIn post was a comment Jordan makes on – what he calls – High-Value Retainers and the effect Gen AI will have on these fee arrangements. To quote:

High-Value Retainers Thanks to Gen AI’s consumption of many traditional tasks, lawyers have moved up the value ladder, going beyond “bet-the-company” and “run-the-company” work to start offering “grow-the-company” work (or “advance-the-individual”). These are engagements in which lawyers ask: “How can I improve your situation? What are your near-term and long-term goals? How can I help you anticipate problems and prevent them before they happen? How can I bring you more stability and peace of mind? How can I be your advocate and counsellor in whatever you need?”

While I think Jordan’s point is an excellent one, mine was this: “Do you think this could work in 10 years time?“

Because if you think it could: Why are you waiting 10 years for AI to develop in order to have this conversation – have this conversation with your clients now!

In that, it’s not a 10+ years from now discussion. It’s not a 10+ years from now problem. It’s a HERE AND NOW problem and a here and now discussion.

In the 1980s it took Concord a little under 3 hours to fly New York to London.

Today [2023], 40 years later, the quickest you can travel that exact same route (New York City – London) is a little over 5 hours.

…And this is why you should always bill by the hour – it ensures your clients get the best possible experience (after all, why would you want to fly Concord!) and it incentives innovation!

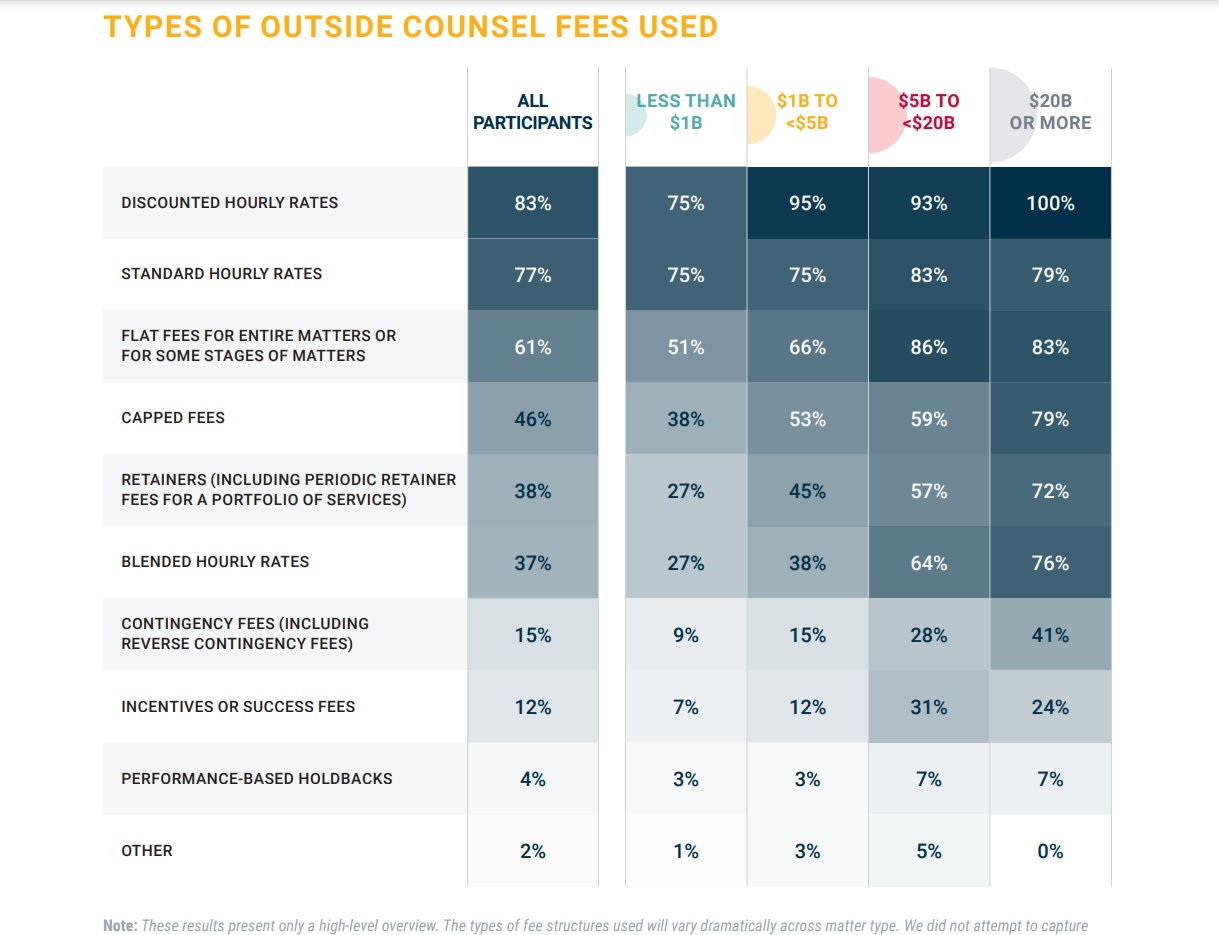

If you are wondering what types of Alternative Fees Arrangements (AFAs) in-house General Counsel are asking their private practice suppliers to provide them with – or, to flip the coin, what AFAs private practice lawyers are charging their in-house GCs, then wonder no longer. The latest market report from the Association of Corporate Counsel (ACC) sets this out in a nice clear table:

Some take-aways:

The #1 AFA fee request of outside counsel is Discounted Hourly Rates. No less than 100% of companies with revenue over $20BN or more use Discounted Hourly Rates with their private practice lawyers! When, oh when, will we learn that Discounted Hourly Rates are NOT a fee structure? On this point, I have been arguing for years (literally, the linked post was from 2018!) that there is no point having a pricing function in your law firm if all you are going to offer clients is discounted hourly rates! Seriously, save yourselves the money.

Say what you want, the #BillableHour is far, far from over if it is the preferred billing method of over three-quarters (77%) of all in-house GCs participants in the survey!

Capped fees are dumb! They are a lose-lose: both for the law firm who if they come under the cap can only charge what is on the clock and if they go over the cap have to wear the additional cost; but also for the in-house team who will get under served as soon as it becomes clear the cap cannot be met (and probably never was going to be). So why are they so prevalent? I can only assume capped fees are driven by the CFO wanting “cost certainty”.

Given the continued popularity of hourly rates, Blended Hourly Rates are nowhere near as popular (at 37%) as you would think. On transactional matters in particular, you would think this rate of use would be a lot higher.

The use of Success Fees is woeful. Is this a reflection of the amount of M&A and privatization work actually being done (where you would expect it to be prevalent, or is it an actual fact that in-house counsel don’t like/understand the benefits of this arrangement? Or could it be, every deal is getting done so why take the uplift risk?)?

An understanding of Performance Based Holdbacks has a long, long way to go.

Importantly though, despite talking about implementing AFAs for over two decades, we are still a long way off actually using them in practice.

Again, take a look at my linked article above where I talk to Patrick Johansen’s Continuum of Fee Arrangements™, where Patrick sets out 16 different types of fee arrangements that can be used:

Hourly

Volume

Blended

Retainer

Capped

Task

Flat

Phase

Fixed

Contingency

Portfolio

Hybrid

Holdback

Risk Collar

Success/Bonus

Value

And ask yourself, how many of these are being actively used in this latest report from the ACC?

Notably missing from the list above? Value Based Billing!

Yes, despite what you may read and hear elsewhere, in practice we are long, long way away from understanding and implementing the appropriate (a term I learned from Toby Brown) use of relevant fee arrangement for the task at hand.

In-house or private practice, if you’re struggling to get to grips with this issue, feel free to reach out to me for a chat.

I have read a lot recently about how AI and ChatGPT in particular is going to kill the billable hour. That may well end up happening. What I do suspect though is that it is unlikely to happen soon. And if the billable hour is to be killed off, technology – such as AI and ChatGPT – may well play a part, but it will be the cultural/behavioural change that’s needed that will be the final nail in this coffin.

Don’t believe me?

Here is a quote (of kinds) by Aarash Darroodi, Fender’s General Counsel, at the recent Legal Marketing Association’s annual gathering in Hollywood, Florida:

…the mere fact that he’s being billed by the hour isn’t a problem — but that the billable hour’s implementation can be.

In other words, Darroodi doesn’t mind that his law firm(s) charge him (his company) by the hour, but he does mind if you take him for a fool.

And until this mindset changes, you’re not going to see the death of the billable hour anytime soon.

Darroodi’s comments on the RFP process – should clients do an “open day” before tendering?

While Darroodi’s comments on the billable hour were interesting, his comments on the approach law firms should take to the RFP process were even more insightful. To quote from the article:

[Darroodi] described receiving template-based RFP responses from law firms — an approach he called “fundamentally a mistake.”

Instead, he would like to see a law firm respond to an RFP with an offer to come look at the company’s operations in-depth, gaining a better picture of his organization before a proposal is prepared.

“First of all, it shows initiative on your part. It shows the fact that you care,” he said. “And plus, it shows us that you’re going to submit something that’s directly related to our existing organization.”

Now I’m more than sure that not all GCs will take this approach. And before everyone in Australia says this would likely breach procurement protocols (after the RFP has been issued), I know.

But, wouldn’t it be interesting – and just a little more relevant, if clients did an “open day” before they issued the RFP? Particularly in cases where the tender is by invitation only?

In my view it would certainly make sense and would undoubtably result in more directly relevant and related (and probably eminently more readable) tender responses.

Not only is it highly insightful – so “thanks for posting it Jeremy”, but it contains this nugget – again from Darroodi – on his views about client events (and if you are anEvents Manager in a law firm, stop reading now 🤣):

“I don’t want to spend time with my lawyers,” Darroodi said to laughter, comparing the idea to hanging out with his dentist.

Ouch!

In the meantime, if you need help with your pricing or RFP responses, feel free to reach out to me.

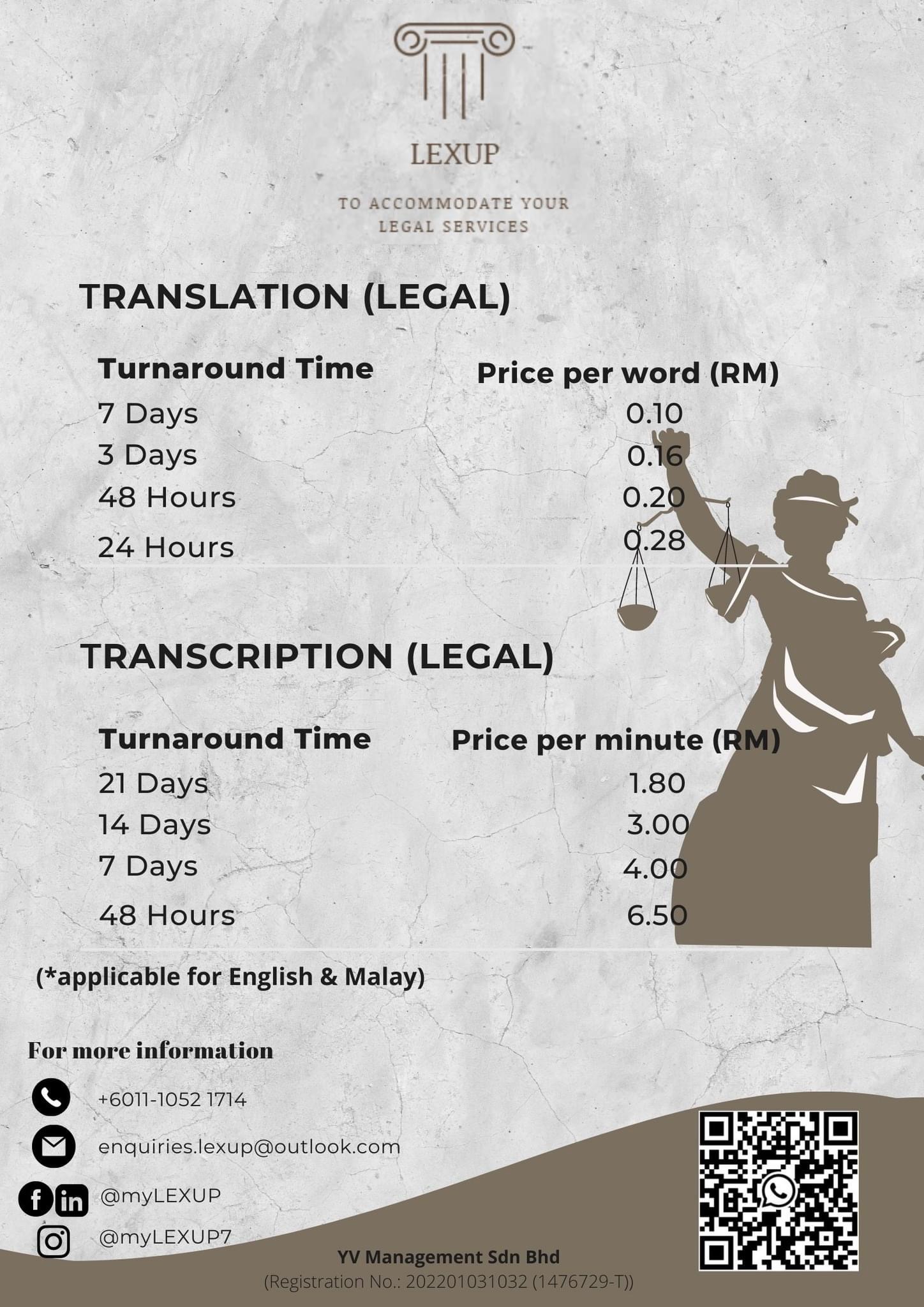

Not exactly sure where I came across this pricing menu by a translation service provider in Malaysia – Lexup – so apologies if I am not giving you the credit you deserve because this really grabbed my attention.

A translation service focussed on the legal profession that not only charges by the minute (let alone 6 minute units), but whose rates vary depending on how urgent your need is.

Alternatively, if you’re not happy with the hourly billing model, then let’s go old school (Charles Dickens era) and pay by the word. Again though, the quicker you want your work back, the more it will cost you!

Peak-load pricing. I have no idea why law firms have not adopted this years ago!

As usual comments are my own – but I’m sure there is someone out there who can tell me the optimum price to time!

In Episode 748 (7 July 2020) of HBR’s Ideacast podcast (23.04), Curt Nickisch interviews Rafi Mohammed, founder of the consulting firm ‘Culture of Profit’, on the topic of ‘Pricing Strategies for Uncertain Times‘.

During the course of the conversation Nickisch states that with COVID-19 service/product providers will be under intense pressure from clients/customers to offer discounts, to which Mohammed replies:

Clearly, in the short-run, you have to offer a discount. And what I would be focused on is what I call discounting with dignity in a manner that doesn’t devalue your product in the long run. And so, that’s really important because once you set a low price, it’s very hard to recover when demand eventually does come back.

And so we turn to how this really important concept applies to law firms

Blind Freddy can tell you that clients are under intense pressure to cut costs. I doubt there is a CFO out there who has not phoned (or even Zoomed) his/her GC and told them to cut costs.

And I suspect there are few GCs out there who have not responded by calling, zooming or even emailing the law firms on their legal panel to tell them to reduce rates by X%.

And, having lived through the Asian Financial Crisis of 1997 and the GFC of 2008, I suspect there are few law firms partners who have not passed along this request to their Finance Department with a note to “make it happen“.

But if this sounds familiar, and if a law partner you know would or has done this (*because it is never us*), then you would be missing out on Mohammed’s very powerful ‘discount with dignity‘ concept.

Because, as much a I hate advocating or agreeing to discounts, Mohammed is right:-

If you offer a discount to customers/clients merely because we are going through turbulent (or should I be saying ‘unprecedented’ 🙂 ) times, then what you are really doing is devaluing your service/product in the long term.

Because what you are saying to your customer/client when you unconditionally agree to a discount request of this kind is that “you have been over paying me all this time” – I’m not really worth what you have been paying me.

A Suggested Alternative Approach

Much like scoping in Legal Project Management methodology, when it comes to discounting (and I’m realistic enough to know that there needs to be some consideration of discounting in current times), you need to be considering what you take out of the basket when you offer that discount.

Which is to say it isn’t a ‘like for like’ for less conversation – you don’t get the same for less. If you take 15% off, you take 15% out of the basket. And you look to alternatives to how that can be sourced – either in-house or some other way (including LPOs/ALSPs).

And, if it really does need to be ‘like for like, but for less’ then it needs to come with a risk sharing collar. For example, I will accept 80% of my fees, but if we get past COVID-19 and your share price returns to pre-COVID highs within 6 months of completing this deal, then you agree to pay me 120% of my fees.

And, in the very worst of scenarios, your invoice should include a line item that states the discount being given is a one-off COVID-19 discount (and Mark Stiving, of Impact Pricing, has an interesting thought on this issue).

Regardless of what it is, you do need to do something. You cannot standstill for less. Because we will get past COVID. And in the ‘new world’ (even if that is a world where we merely live with COVID) there will be a ‘new, new normal’. And if you have agreed to discount your rates now without taking anything out of the basket, then what you have actually done is recalibrated your value in the new world.

And you won’t recover from that.

As always, the above just represent my own thoughts and would love to hear your thoughts.

For those who have not read it, Izaret and Schurmann’s Whitepaper provides some really thought-provoking insights, including:

Progressive pricing scales prices up or down on the basis of the value an individual customer derives.

the levels of pricing under progressive pricing are value-based, not means-based

Progressive pricing seems to violate the rules of traditional economics, which assume that customers buying the same product or service will pay the same price.

Progress pricing enables providers to offer each customer a fair, personalized product and price point.

In essence, progressive pricing enables service providers, such as law firms, to calibrate the value they provide at an individual customer level.

But, importantly to Izaret and Schurmann (see #4 of their ‘four most important differences between progressive and traditional pricing approaches‘):

Progressive pricing is a fairer way to determine prices, because customers pay a price proportional to the value they receive, rather than paying the same fixed price others pay.

For any supporters of value-based pricing, the above quote is pure gold.

But, the caveat in next line of Izaret and Schurmann’s piece is probably more crucial:

But the firm must make the case for this perceived fairness

QED, it is the duty of the firm to communicate the value the customer is getting, not the customer!

As a growing advocate of value-based pricing in professional services, one of the greatest take-outs for me was this line:

Making progressive pricing a profitable day-to-day reality can happen only if firms change how they create, define, and measure value so that they can share it fairly.

All I can say to that is “amen” – because it isn’t going to come out of utilisation and realisation rates, no matter how hard you look!

It is such a great piece I’m going to leave you with the following three quotes from this paper:

Companies must first step back and re-imagine the concept of value in their market. How can a business combine its own capabilities with the close personal knowledge of its customers to create something that fundamentally changes a customer’s life?

Can you define value, measure it, and get everyone to agree on what value is?

Most firms are accustomed to expressing prices in units of product or some other basic metric such as hours. If they can instead calibrate prices in terms of unit of value, then the price per unit of value can remain constant and the amount a customer pays can scale in proportion to the value demanded. That is the essence of fairness.

Great read. If it is not on your list – add it* (*then get back to me and let me know if you agree)!