The most recent Wells Fargo report on the state of the US market has just been published. While obviously US centric, I’m sure many of the trends are being reflected elsewhere, so worth a look.

𝗦𝘁𝗿𝗼𝗻𝗴 𝗶𝗻𝗱𝘂𝘀𝘁𝗿𝘆 𝗽𝗲𝗿𝗳𝗼𝗿𝗺𝗮𝗻𝗰𝗲 𝗱𝗲𝘀𝗽𝗶𝘁𝗲 𝘂𝗻𝗰𝗲𝗿𝘁𝗮𝗶𝗻𝘁𝘆

Global economic and geopolitical volatility has not slowed Big Law growth (so far)

Rates increased ~𝟭𝟭–𝟭𝟮%, the primary contributor to revenue growth

So far, minimal client pushback despite sustained increases

𝗖𝗼𝗹𝗹𝗲𝗰𝘁𝗶𝗼𝗻𝘀 𝗮𝗻𝗱 𝗰𝗮𝘀𝗵 𝗳𝗹𝗼𝘄 𝗲𝗺𝗲𝗿𝗴𝗶𝗻𝗴 𝗮𝘀 𝗮 𝗿𝗶𝘀𝗸

Collection cycle have slowed (~6.5 days longer)

Inventory (unbilled/uncleared work) is rising faster than revenue

End-of-year performance will depend on converting work to cash

𝗢𝗽𝗲𝗿𝗮𝘁𝗶𝗼𝗻𝗮𝗹 𝘁𝗿𝗲𝗻𝗱𝘀

Productivity is up modestly (+1.2%)

Headcount growth is steady (~3.3%)

Expenses are rising (especially in senior staff and technology)

𝗠𝘆 𝘁𝗵𝗿𝗲𝗲 𝘁𝗮𝗸𝗲𝗮𝘄𝗮𝘆𝘀

𝟭. The impact AI is having on demand is still minimal (actually, it is increasing work on the demand side!). On the productivity side, this may change, but increase demand is, so far, taking up any excess capacity. This (as well as the other indicators in the report) most likely means the Billable Hour will still be with us for some time to come.

𝟮. Realisation rates and increased collections times should be a real concern. No point charging $1,000 an hour if you never get paid!

𝟯. Amen to this!! – many firms have figured that rates are part of their branding, “and it’s very short-term thinking to try and manipulate rates downward to offset a decrease in demand.”

The most recent – 2026 – Citi Hilderbrandt Client Advisory Survey Report published earlier this month contains some interesting commentary on how US law firms faired in 2025. None more so than the finding that:

a growing number of firms estimating that more than half their revenue will come from pre-negotiated discounts. (page 23)

Pre-negotiated discounts

The Report does not explicitly define “pre-negotiated discounts”; however it refers to alternative fee arrangements (AFAs) as including fixed, capped or blended rates. It is, therefore, reasonable to interpret “pre-negotiated discounts” as encompassing agreed reductions to standard charge-out rates, volume-based discounts and other upfront pricing concessions.

Viewed positively, this trend signals a shift away from reactive, end-of-matter discounting towards earlier and more deliberate pricing discussions. In principle, this should create a stronger foundation for meaningful conversations about value-based pricing, particularly where clients are seeking price certainty, predictability and risk sharing. From that perspective, pre-negotiated pricing is not inherently problematic — and may in fact represent a necessary transitional step.

The more concerning implication, however, is that for many firms these discussions appear to be anchored primarily in discounting, rather than in value definition. Where pricing conversations begin and end with rate reductions, firms risk reinforcing a price-taker mindset rather than asserting their role as price-setters. Left unchallenged, this dynamic contributes to margin erosion, commoditisation of legal services and an imbalance in client-firm relationships that becomes increasingly difficult to unwind.

AFAs as a pricing option

Despite persistent commentary throughout 2025 that artificial intelligence (ai) will fundamentally disrupt — or even eliminate — the billable hour, the data in this Report suggests otherwise. The proportion of revenue derived from AFAs has remained effectively flat, increasing only marginally from 23.5% in 2024 to a projected 23.6% in 2025.

Setting aside the fact that many commonly cited AFAs are, in reality, variations of the billable hour by another name, and acknowledging that it may still be too early to fully assess AI’s structural impact on pricing legal services, one conclusion is unavoidable: the billable hour remains very much alive.

The way forward

With 74% of firms expecting a growing proportion of revenue to come from AFAs by 2027, the issue is not whether pricing models will continue to evolve, but how deliberately firms choose to engage with that evolution; and whether AFAs are used as strategic tools or simply as discounted billing mechanisms.

In sum

Taken together, the findings in this Report further highlight a profession at an inflection point. While the billable hour continues to dominate, the steady rise of pre-negotiated discounts and the anticipated growth in AFAs suggest mounting client pressure for greater certainty, transparency and perceived value.

The critical question for law firms now is not whether they should offer alternative pricing arrangements, that horse has bolted, but whether they are prepared to move beyond discount-led negotiations and engage in genuine upfront value-based pricing conversations.

Firms that continue to compete primarily on price risk entrenching themselves as price-takers in an increasingly sophisticated procurement environment. Those that invest in articulating value, pricing outcomes and structuring risk intelligently will be far better positioned to protect margins and strengthen client relationships in the years ahead.

The decision on the way forward now rests with the firms themselves.

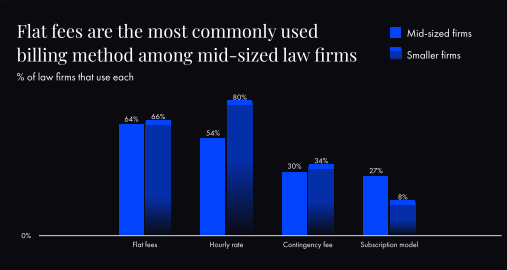

Clio’s 2025 Legal Trends Report for Mid-Sized Law Firms provides a comprehensive look at how mid-sized law firms in the US are adapting to industry changes; particularly as it relates to AI adoption, billing models, client acquisition, and technology investments.

Although the results are based on data from US-based firms, the results are arguably applicable here in Australia and more broadly so here’s a summary of the key takeaways:

🚀 AI Adoption & Transformation

Mid-sized firms (20+ employees) are now leading AI adoption in legal tech, surpassing smaller firms.

93% of surveyed professionals in these firms use AI, with 51% using it widely or universally.

Common AI tools include legal research platforms, document automation, eDiscovery, and predictive legal analytics.

AI is viewed as a way to increase efficiency, reduce costs, and improve client engagement.

💰 Billing Models & Pricing Trends

Flat fees are now the most common billing method among mid-sized firms, outpacing hourly rates.

Firms are shifting away from hourly billing due to AI’s impact on time-based work and client preference for predictable pricing.

Subscription models are also gaining traction, especially for ongoing legal services to business clients.

Despite the shift, hourly billing remains prevalent, particularly with highly varied rates by role and experience.

📈 Client Acquisition & Marketing Strategies

Mid-sized firms use multiple marketing channels: websites, SEO consultants, social media, online reviews, and referrals.

They’re less reliant on referrals than smaller firms, but invest more in digital marketing.

Tools like e-signatures, intake forms, and online scheduling directly improve conversion rates and revenue (up to 20% higher).

Chatbots are underused despite 51% of clients finding them helpful—a missed opportunity.

💸 Spending & Technology Investments

Staff salaries dominate expenses (41%), followed by rent, marketing, and office costs.

Mid-sized firms spend less on office expenses (5%) than solo and smaller firms, due to economies of scale and flexible work arrangements.

Spending on software and professional fees is rising rapidly—showing a strong focus on tech and professional development.

☁️ Cloud Technology Adoption

Mid-sized firms lag behind smaller firms in cloud adoption (only 38% vs. 71%).

Firms with 20–49 employees are more likely to use cloud tools than larger mid-sized firms.

Hesitation around switching legacy systems or internal decision-making bottlenecks may be holding back adoption.

🧭 Strategic Takeaways

Mid-sized firms embracing AI + modern billing models + tech investments are poised to outpace competitors.

The real threat isn’t automation—it’s firms that adapt faster.

Cloud-based tools, client intake tech, and AI are critical for efficiency, growth, and client satisfaction.

The latest Law Society (England and Wales) Financial Benchmarking Survey has sparked significant discussion on social media today. The findings highlight some critical financial challenges for mid-sized law firms, particularly in terms of profitability, chargeable hours and cash flow management.

📊 Top 3 Key Findings:

1️⃣ Fee Earners’ Costs vs. Fees Charged

The median hourly cost of a fee earner (based on 1,100 chargeable hours) was £123.40, while the median hourly fees per fee earner stood at £133.01.

🔴 93% of fees earned are being used to cover costs, leaving minimal margin for profitability.

2️⃣ Shortfall in Chargeable Hours

The average recorded chargeable hours per fee earner increased slightly to 773 hours (up from 765 in 2023).

⚠️ However, this is still well below the 1,100-hour target—a shortfall of over 300 hours per year per lawyer.

3️⃣ Increase in Lock-Up Days

Year-end lock-up days (including work in progress and debtors) rose from 143 to 146 days.

This trend indicates longer cash flow cycles, which can put pressure on a firm’s financial stability.

🚨 What Should Law Firms Do?

These figures underscore the urgent need for better financial planning, sustainable profitability strategies, and operational efficiency. Some key focus areas include:

✔️ Improving revenue streams—exploring retainer-based models for better income predictability. ✔️ Enhancing productivity—have a robust and actionable business development plan for all lawyers! ✔️ Optimise cash flow—reduce lock-up days by streamlining billing and collections processes.

📢 Looking to bridge the 300+ hour gap per lawyer? Or interested in strategies for growing a profitable legal practice sustainably? Let’s talk! Get in touch today.

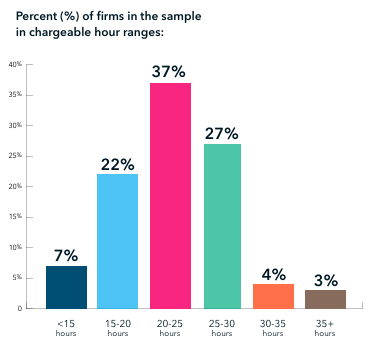

A recent report, “Strategic Sector Insights for the Legal Profession 2025: Mid-Sized Firms”, published by The Law Society and MHA, reveals a striking trend:

👉 More than 50% of mid-sized law firms report that their lawyers bill less than 25 hours per week on average. 👉 Less than 3% of lawyers at these firms bill anywhere close to the full 40-hour workweek.

While it’s unrealistic to expect lawyers to bill every hour they work, these numbers highlight why alternative pricing models are a key priority for firm leaders in 2025.

⚖️ What does the future of legal pricing look like? If you’re exploring value-based pricing, subscription models, or hybrid fee structures, let’s talk!

📩 DM me to discuss innovative pricing strategies for law firms.

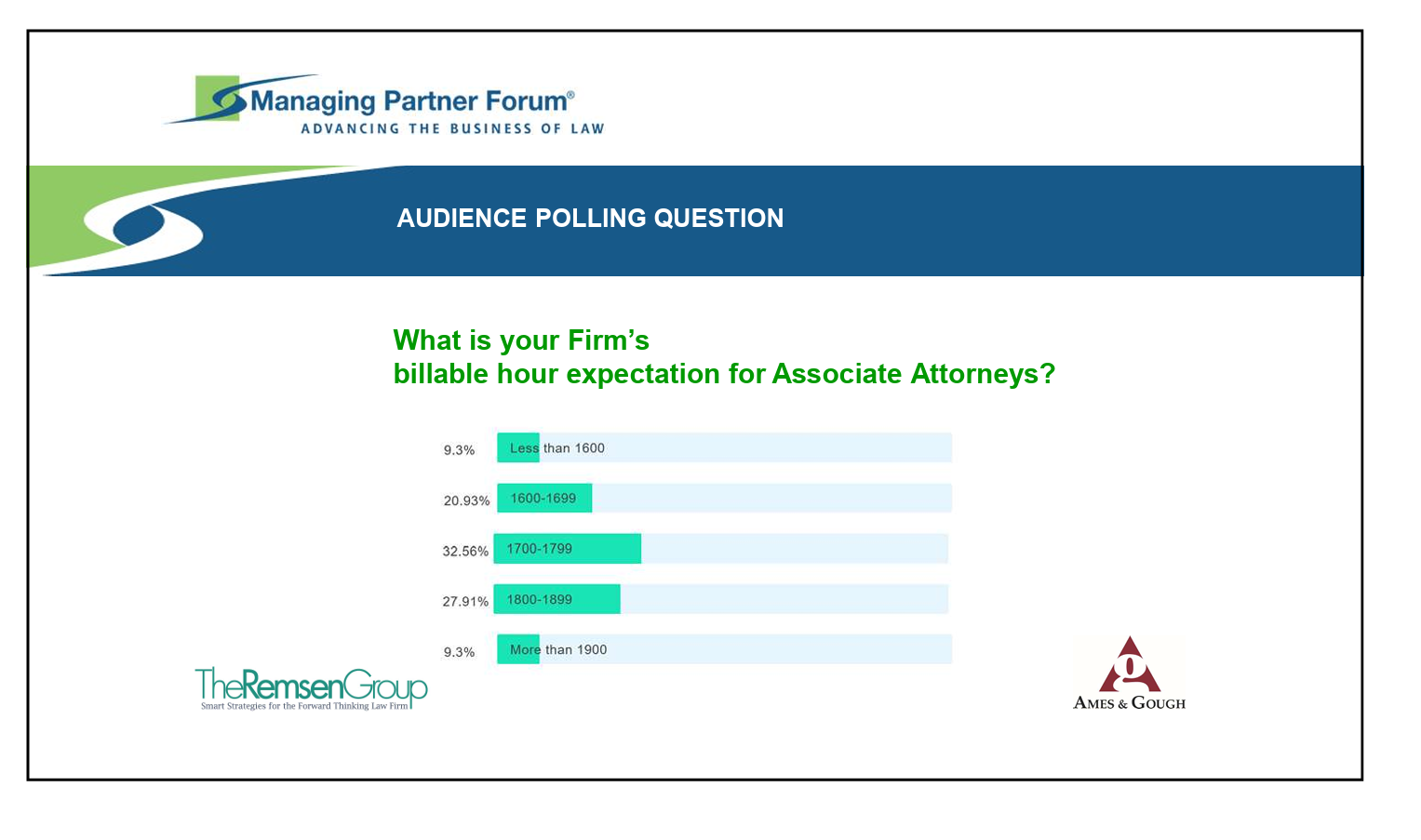

It’s interesting to note that nearly 70% of respondents expect their Associate Attorneys to bill over 1700 hours a year, with almost 10% expecting over 1900 billable hours per year.

That’s a lot of billable hours! And if we consider the ‘10-20-30-40 Leverage Rule‘, then the implication is very bleak for junior lawyers!

And as I say to those entering the legal profession who need some understanding of how many hours they need to work to meet their billable hour target, take a look at Yale Law School’s ‘The Truth About The Billable Hour‘.

While I am all for the profit motive, I maintain that if owners and managers of law firms want to understand why they have a high attrition / burnout rate in their teams, take a close look at what expecting someone to bill 1700 hours a year is actually doing to them!

As we start out on 2025, the 𝑨𝒖𝒔𝒕𝒓𝒂𝒍𝒊𝒂𝒏 𝑭𝒊𝒏𝒂𝒏𝒄𝒊𝒂𝒍 𝑹𝒆𝒗𝒊𝒆𝒘 (AFR) has helpfully published a table today (14.01.2025) – ‘𝐁𝐢𝐥𝐥𝐚𝐛𝐥𝐞 𝐡𝐨𝐮𝐫𝐬 𝐭𝐚𝐫𝐠𝐞𝐭𝐬 𝐟𝐨𝐫 𝐟𝐢𝐫𝐬𝐭-𝐲𝐞𝐚𝐫 𝐥𝐚𝐰𝐲𝐞𝐫𝐬 𝐚𝐭 𝐬𝐞𝐥𝐞𝐜𝐭𝐞𝐝 𝐥𝐚𝐰 𝐟𝐢𝐫𝐦𝐬’ – that makes for very interesting reading.

Other than the expected billable hour targets for first year lawyers and comments on alleged “under-billing” practices at major Australian law firms, what caught my attention in the article was this comment:

I might be wrong, but in the event that Hamilton Locke charges clients by the billable hour, then I highly suspect this also translates into a yearly hourly target…

…In the event that HL charges clients fixed fees or some other type of fee arrangement, then I accept this calculation probably sets it apart.

The Association of Corporate Council (ACC) – the worldwide association that promotes the interests of in-house counsel – recently published its ‘10 Key Findings from the ACC CLO Survey 2024‘.

While I have not read the full report, there are some very interesting take-outs from the Executive Summary, including:

58 percent of [in-house] departments have been impacted by law firm rate hikes

42 percent of CLOs say their legal department received a cost cutting mandate over the past year

23 percent of in-house say that rate increases have been difficult to manage

only 9 percent are “very confident” in their organization’s ability to mitigate emerging data risks

The top 3 issues that keep CLOs up at night are not what you would think [well, maybe one of them!]

The importance of ESG would appear to be a little over cooked – but…

…I’ll leave you with this one: 63 percent of CLOs say they are seeking to develop greater business acumen among the lawyers in their department – Good luck with that one!

Check out the link above to read more and as always if need any help feel free to get in touch.