The number of senior business development people, including Director level roles, I have spoken to over the years who “fell” into working in business development roles for professional services firms is remarkable! Yes, in most cases they had a relevant applicable skill-set that could be transferred and used in the new role: whether that be as an ex-lawyer, marketing graduate or communications professional; but, by and large, I think it’s fair to say that almost none of us saw a career advisor at school and asked what undergraduate and post graduate degrees we need in order to have a career in business development for a professional services firm*.

So I was really glad to read today, via the Legal Cheek blog, that Slaughter and May are to launch a business services grad scheme.

Although Slaughters are one of the few Magic Circle firms I never worked at or for, I have really admired them from the sidelines. Their focus on their core strategy is commendable. All of which, in my opinion, is reflected in their newly announce two year ‘Business Services Academy‘ program.

In a similar vein to grad rotations, Legal Cheek is reporting that the Academy program will consist of four rotations of six months each among:

- people and operations

- technology legal ops and project management; and

- clients and business development.

Now, the very clever people you are, you’re think 4 into 3 doesn’t go – and you would be right. But, apparently the forth rotation is with the team you have enjoyed the most on your previous rotations and want to consider a career with, and I kind of like that!

So once again, the team at Slaughter and May are blazing a path, but please do we really need to say this:

It’s worth noting that this scheme does not lead to qualification as a solicitor.

Anyhow, if you are not fortunate enough to work at Slaughters – or, as Legal Cheek points out Addleshaw Goddard or DWF (who have similar programs), and really need to learn a thing or two about how business development in law firms actually works in practice, reach out to me!

* I would also add that a lot of that same thinking applies to lawyers trying to do business development, in that they have had no formal training in this skill!

This second graph looks numbers of hours worked per lawyer and this looks to have flat-lined since the GFC in 2008. So no real change there.

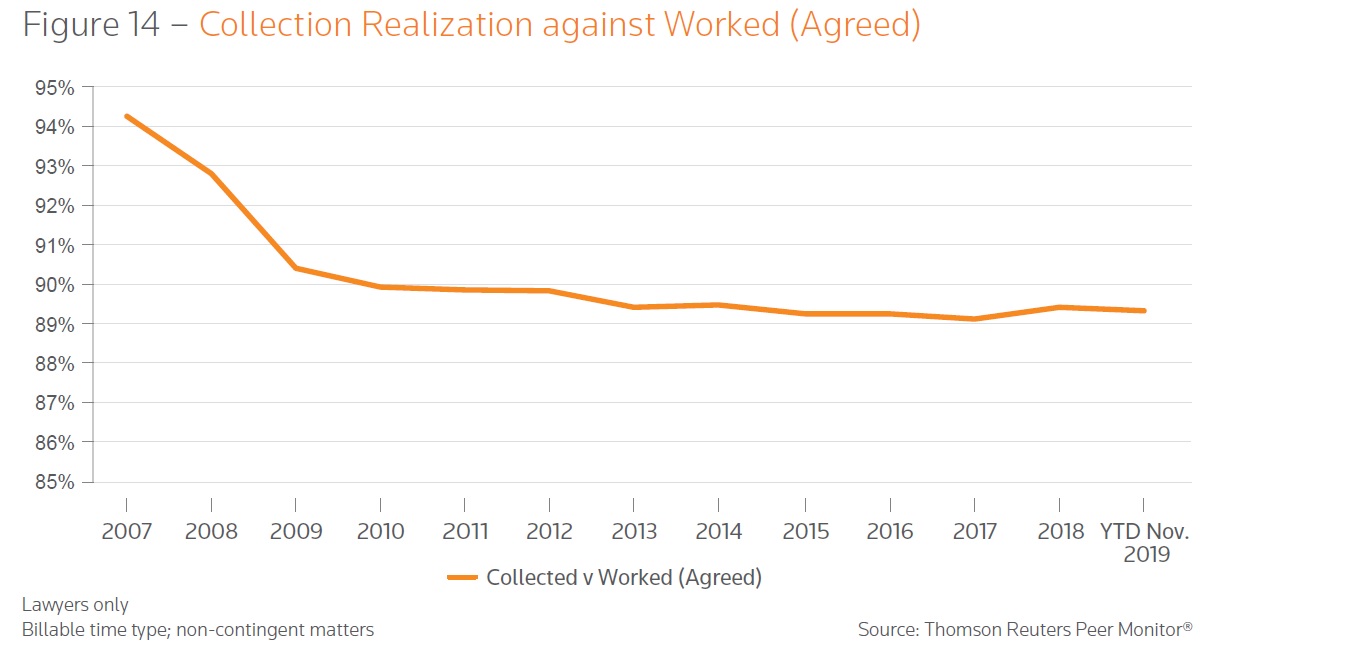

This second graph looks numbers of hours worked per lawyer and this looks to have flat-lined since the GFC in 2008. So no real change there. This third – and last – graphic looks at collection realization against agreed worked and, again, has pretty much flat-lined over the past 5 years at a relatively horrid 89.5%.

This third – and last – graphic looks at collection realization against agreed worked and, again, has pretty much flat-lined over the past 5 years at a relatively horrid 89.5%.