The most recent – 2026 – Citi Hilderbrandt Client Advisory Survey Report published earlier this month contains some interesting commentary on how US law firms faired in 2025. None more so than the finding that:

a growing number of firms estimating that more than half their revenue will come from pre-negotiated discounts. (page 23)

Pre-negotiated discounts

The Report does not explicitly define “pre-negotiated discounts”; however it refers to alternative fee arrangements (AFAs) as including fixed, capped or blended rates. It is, therefore, reasonable to interpret “pre-negotiated discounts” as encompassing agreed reductions to standard charge-out rates, volume-based discounts and other upfront pricing concessions.

Viewed positively, this trend signals a shift away from reactive, end-of-matter discounting towards earlier and more deliberate pricing discussions. In principle, this should create a stronger foundation for meaningful conversations about value-based pricing, particularly where clients are seeking price certainty, predictability and risk sharing. From that perspective, pre-negotiated pricing is not inherently problematic — and may in fact represent a necessary transitional step.

The more concerning implication, however, is that for many firms these discussions appear to be anchored primarily in discounting, rather than in value definition. Where pricing conversations begin and end with rate reductions, firms risk reinforcing a price-taker mindset rather than asserting their role as price-setters. Left unchallenged, this dynamic contributes to margin erosion, commoditisation of legal services and an imbalance in client-firm relationships that becomes increasingly difficult to unwind.

AFAs as a pricing option

Despite persistent commentary throughout 2025 that artificial intelligence (ai) will fundamentally disrupt — or even eliminate — the billable hour, the data in this Report suggests otherwise. The proportion of revenue derived from AFAs has remained effectively flat, increasing only marginally from 23.5% in 2024 to a projected 23.6% in 2025.

Setting aside the fact that many commonly cited AFAs are, in reality, variations of the billable hour by another name, and acknowledging that it may still be too early to fully assess AI’s structural impact on pricing legal services, one conclusion is unavoidable: the billable hour remains very much alive.

The way forward

With 74% of firms expecting a growing proportion of revenue to come from AFAs by 2027, the issue is not whether pricing models will continue to evolve, but how deliberately firms choose to engage with that evolution; and whether AFAs are used as strategic tools or simply as discounted billing mechanisms.

In sum

Taken together, the findings in this Report further highlight a profession at an inflection point. While the billable hour continues to dominate, the steady rise of pre-negotiated discounts and the anticipated growth in AFAs suggest mounting client pressure for greater certainty, transparency and perceived value.

The critical question for law firms now is not whether they should offer alternative pricing arrangements, that horse has bolted, but whether they are prepared to move beyond discount-led negotiations and engage in genuine upfront value-based pricing conversations.

Firms that continue to compete primarily on price risk entrenching themselves as price-takers in an increasingly sophisticated procurement environment. Those that invest in articulating value, pricing outcomes and structuring risk intelligently will be far better positioned to protect margins and strengthen client relationships in the years ahead.

The decision on the way forward now rests with the firms themselves.

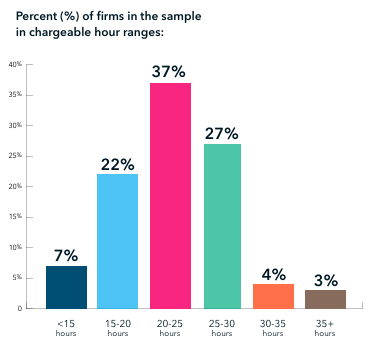

A recent report, “Strategic Sector Insights for the Legal Profession 2025: Mid-Sized Firms”, published by The Law Society and MHA, reveals a striking trend:

👉 More than 50% of mid-sized law firms report that their lawyers bill less than 25 hours per week on average. 👉 Less than 3% of lawyers at these firms bill anywhere close to the full 40-hour workweek.

While it’s unrealistic to expect lawyers to bill every hour they work, these numbers highlight why alternative pricing models are a key priority for firm leaders in 2025.

⚖️ What does the future of legal pricing look like? If you’re exploring value-based pricing, subscription models, or hybrid fee structures, let’s talk!

📩 DM me to discuss innovative pricing strategies for law firms.

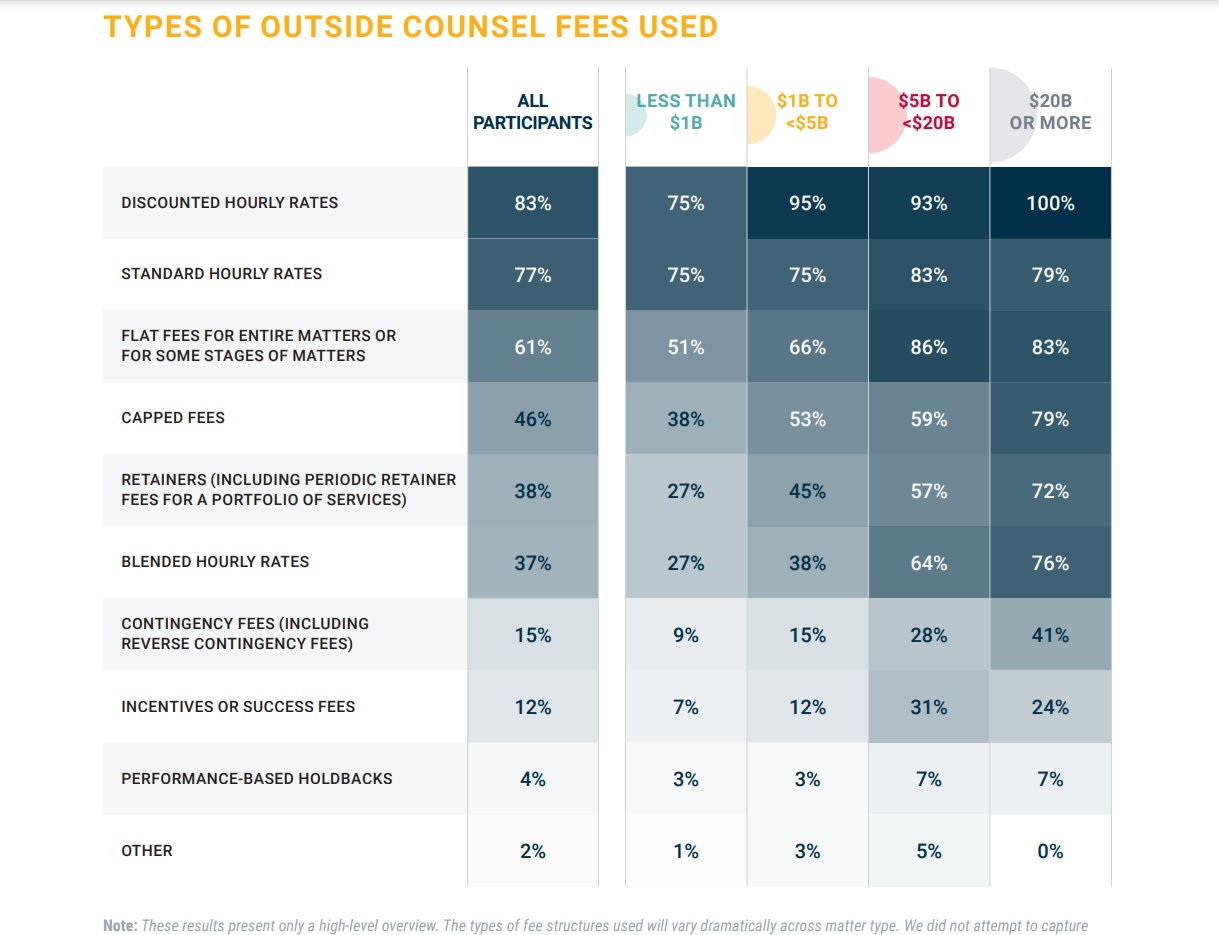

If you are wondering what types of Alternative Fees Arrangements (AFAs) in-house General Counsel are asking their private practice suppliers to provide them with – or, to flip the coin, what AFAs private practice lawyers are charging their in-house GCs, then wonder no longer. The latest market report from the Association of Corporate Counsel (ACC) sets this out in a nice clear table:

Some take-aways:

The #1 AFA fee request of outside counsel is Discounted Hourly Rates. No less than 100% of companies with revenue over $20BN or more use Discounted Hourly Rates with their private practice lawyers! When, oh when, will we learn that Discounted Hourly Rates are NOT a fee structure? On this point, I have been arguing for years (literally, the linked post was from 2018!) that there is no point having a pricing function in your law firm if all you are going to offer clients is discounted hourly rates! Seriously, save yourselves the money.

Say what you want, the #BillableHour is far, far from over if it is the preferred billing method of over three-quarters (77%) of all in-house GCs participants in the survey!

Capped fees are dumb! They are a lose-lose: both for the law firm who if they come under the cap can only charge what is on the clock and if they go over the cap have to wear the additional cost; but also for the in-house team who will get under served as soon as it becomes clear the cap cannot be met (and probably never was going to be). So why are they so prevalent? I can only assume capped fees are driven by the CFO wanting “cost certainty”.

Given the continued popularity of hourly rates, Blended Hourly Rates are nowhere near as popular (at 37%) as you would think. On transactional matters in particular, you would think this rate of use would be a lot higher.

The use of Success Fees is woeful. Is this a reflection of the amount of M&A and privatization work actually being done (where you would expect it to be prevalent, or is it an actual fact that in-house counsel don’t like/understand the benefits of this arrangement? Or could it be, every deal is getting done so why take the uplift risk?)?

An understanding of Performance Based Holdbacks has a long, long way to go.

Importantly though, despite talking about implementing AFAs for over two decades, we are still a long way off actually using them in practice.

Again, take a look at my linked article above where I talk to Patrick Johansen’s Continuum of Fee Arrangements™, where Patrick sets out 16 different types of fee arrangements that can be used:

Hourly

Volume

Blended

Retainer

Capped

Task

Flat

Phase

Fixed

Contingency

Portfolio

Hybrid

Holdback

Risk Collar

Success/Bonus

Value

And ask yourself, how many of these are being actively used in this latest report from the ACC?

Notably missing from the list above? Value Based Billing!

Yes, despite what you may read and hear elsewhere, in practice we are long, long way away from understanding and implementing the appropriate (a term I learned from Toby Brown) use of relevant fee arrangement for the task at hand.

In-house or private practice, if you’re struggling to get to grips with this issue, feel free to reach out to me for a chat.

I have read a lot recently about how AI and ChatGPT in particular is going to kill the billable hour. That may well end up happening. What I do suspect though is that it is unlikely to happen soon. And if the billable hour is to be killed off, technology – such as AI and ChatGPT – may well play a part, but it will be the cultural/behavioural change that’s needed that will be the final nail in this coffin.

Don’t believe me?

Here is a quote (of kinds) by Aarash Darroodi, Fender’s General Counsel, at the recent Legal Marketing Association’s annual gathering in Hollywood, Florida:

…the mere fact that he’s being billed by the hour isn’t a problem — but that the billable hour’s implementation can be.

In other words, Darroodi doesn’t mind that his law firm(s) charge him (his company) by the hour, but he does mind if you take him for a fool.

And until this mindset changes, you’re not going to see the death of the billable hour anytime soon.

Darroodi’s comments on the RFP process – should clients do an “open day” before tendering?

While Darroodi’s comments on the billable hour were interesting, his comments on the approach law firms should take to the RFP process were even more insightful. To quote from the article:

[Darroodi] described receiving template-based RFP responses from law firms — an approach he called “fundamentally a mistake.”

Instead, he would like to see a law firm respond to an RFP with an offer to come look at the company’s operations in-depth, gaining a better picture of his organization before a proposal is prepared.

“First of all, it shows initiative on your part. It shows the fact that you care,” he said. “And plus, it shows us that you’re going to submit something that’s directly related to our existing organization.”

Now I’m more than sure that not all GCs will take this approach. And before everyone in Australia says this would likely breach procurement protocols (after the RFP has been issued), I know.

But, wouldn’t it be interesting – and just a little more relevant, if clients did an “open day” before they issued the RFP? Particularly in cases where the tender is by invitation only?

In my view it would certainly make sense and would undoubtably result in more directly relevant and related (and probably eminently more readable) tender responses.

Not only is it highly insightful – so “thanks for posting it Jeremy”, but it contains this nugget – again from Darroodi – on his views about client events (and if you are anEvents Manager in a law firm, stop reading now 🤣):

“I don’t want to spend time with my lawyers,” Darroodi said to laughter, comparing the idea to hanging out with his dentist.

Ouch!

In the meantime, if you need help with your pricing or RFP responses, feel free to reach out to me.

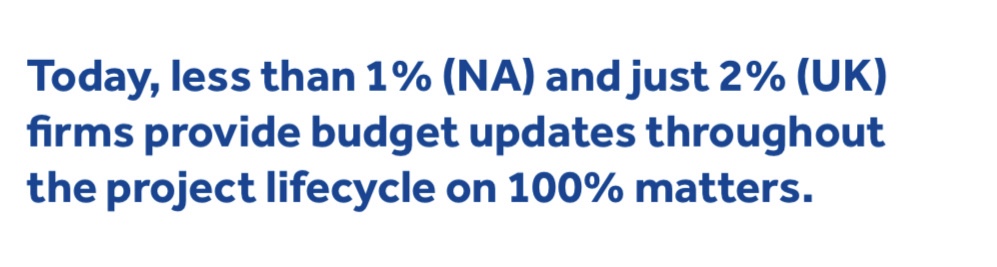

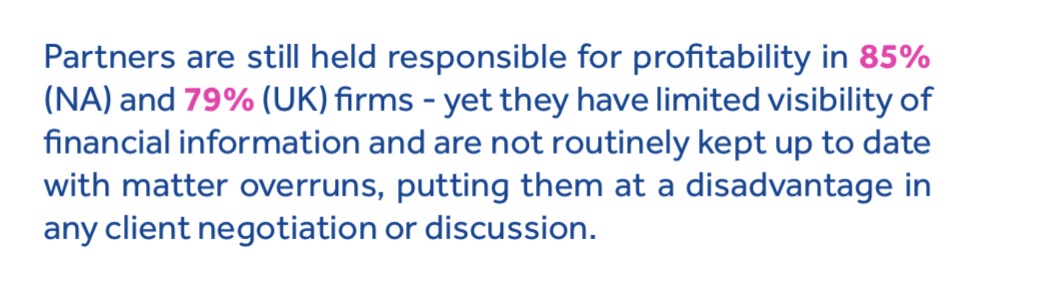

I’m a cynic, so usually read industry reports published by industry providers with a huge pinch of salt, but every now and then you get an exception to the rule. So is the case with BigHand’s recently published ‘The Legal Pricing & Budgeting Report’, which is full of really insightful information (so read it!).

Here are my 10 take-outs (NA = North America and UK = UK):-

From

The damning:

1.

To the surprising:

2.

3.

To some obvious:

4.

5.

And some knowns:

6.

7.

With a few, “What the?” (as in, only…)

8.

9.

With a great conclusion:

10.

As I said, as a rule I don’t recommended reading these types of reports as they typically are a waste of time; but this is one I have no problem saying “go read it!” – and if you have any thoughts/comments, post them in the comments section below!

‘What would be some of the things I would want to be looking out for in a law firm’s invoice?

So here’s a quick list of my 10 things, but feel free to add your own 🤪 :-

Being charged [for]:

Expenses/disbursement – especially if they are unaccounted for (and particularly on fixed fee matters)

Travel time – especially if your lawyer is in the same town/city as you

‘Reading in’ time – especially when a new lawyer joins the team because one of the original team members has resigned or left the team

Team meetings to discuss your case/matter

Multiple lawyers attending the same meeting – especially if they have different time eateries

‘Out of scope’ work without a corresponding change order

Block billing of numerous tasks without explanation

Promotions – charge-out rates being increased for lawyers on your case because they have gain an additional year of post-qualified experience without adding any additional value

‘Bill padding’/‘Rounding up’ – when your lawyer rounds their time up to the next billable unit

‘Stickiness’ – where senior lawyers are doing work on your file that could be easily have been done by more junior lawyers, but they do it because they need to meet their internal billable targets.have different time.

As I say, feel free to add some of your own in the comments.

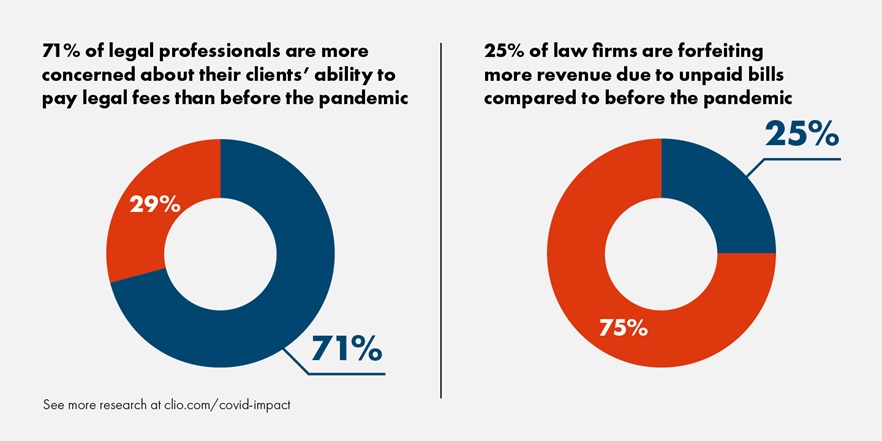

Having reported a cliff-fall in new matter instructions post-COVID in its Legal Trends ReportBriefing #1 in May of this year, June’s updated Briefing #2 by Clio shows a subsequent significant upward spike in new matter instructions that have, effectively, netted out year-on-year the number of new file matter instructions.

While, at first glance, a return to quasi-normal file opening matter numbers look to be good news for law firms, as the latest Briefing numbers also shows, if you scratch the surface you’ll soon see (diagram below) a far bigger underlying problem is starting to emerge – namely clients’ inability (or possibly unwillingness) to pay!

While the above wheel-chart is, at first glance, alarming, it’s also worth keeping in mind that a client’s ‘ability‘ to pay a legal fee pre and post the pandemic is not necessarily the same as its ‘willingness‘ to pay that fee. Which is to say there may be (and likely are) other underlying reasons as to why clients are saying they are not willing to pay fees – including a re-evaluation on the part of the client in respect of the perceived value being provided.

Of more concern to law firm management, however, should lie in the second of these two charts, namely the fact that rather than chasing fees 25% of firms are electing to forfeit the revenue.

Again, there could be a whole raft of underlying reasons why a firm may decide it would rather forfeit some of its billed revenue, and without undertaking a root-cause analysis we left to guess these (including my favourite – trying to preserve the relationship), but we should be left under no illusion that discounting and write-offs will have the biggest impact on profitability*.

A willingness to look at alternative payment methods

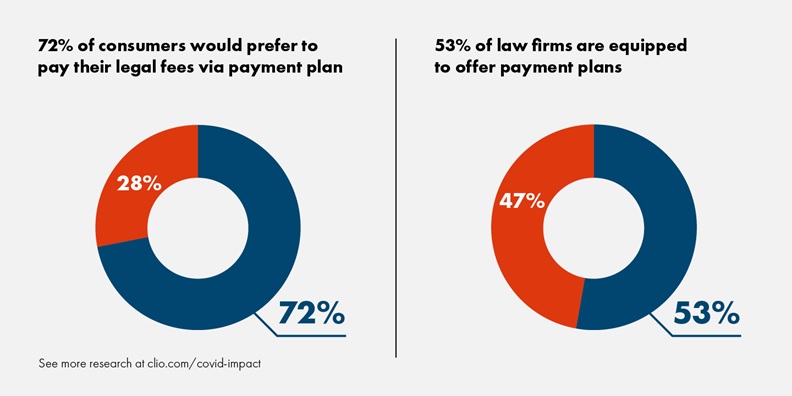

For me, a somewhat surprising take-out from the latest Briefing was the statistic that 72% of consumers would prefer to pay their legal fees via a payment plan. Again, the term “consumer” isn’t defined and so we are left wondering if this is B2C or B2B; but even then, that only 53% of firms are equipped to offer payment plans seems odd.

Take away?

So what’s my top 3 take outs from this latest Briefing from Clio?

Once things settle down, law firms will be as busy as ever,

Cashflow will be king and clients are struggling with their own cash-flow, so

Think outside of the box when it comes to pricing and how you ask clients to pay and you should be okay.

As always, these just represent my thoughts and always interested to hear your views.

* N.B. If hourly billing is the way you work and you want to get a better understanding of the effect that discounting/write-offs has on your firm’s profitability, take a look at this post by Patrick Johansen that profiles Stuart Dodds’ ‘1-3-4 Rule‘

Annuity revenue – a predictable revenue stream from new or existing customers who buy products and services associated with new or previously purchased products.

As the Managing Partner of a law firm today, what would you say if I walked into your office and told you that I could:

provide you with a guaranteed monthly revenue income,

with a product that creates loyal customers, and

where those customers become – at no additional cost to you – brand champions and refer your services to their network, free of charge, via the Holy Grail of marketing – positive ‘word of mouth’ referrals.

Sounds great doesn’t it. Almost too good to be true.

Well all I can say is that if you were anything like one of the Managing Partners servicing customers who responded to the Pitcher Partners recent ‘Legal Survey 2020 Report‘, that’s exactly what you would be saying: “thanks, but no thanks we are happy with the billable hour”.

The fact that the billable hour remains the ‘go to’ method of billing (not the same as pricing) for Australian law firms and their customers does not, in and of itself, surprise me. I must admit, however, to being a little surprised with the 1% increase in this billing method (up from 58% to 59%) year-on-year.

Given the times (even pre Covid-19), I was also a little surprised to see that both ‘fixed fee’ and ‘value-based’ pricing remain relatively static (although it should be added that from what I could see the report lacks a definition of ‘value-based’, probably purposely so).

To me this represents a massive lack of foresight on the part of law firms and a significant lost opportunity.

In much the same way as software as a service (SaaS) companies have come to realise that one-off payments around shrink wrap contracts were not servicing the long-term financial interests of the company (unless it’s a legacy product that will no longer be supported), the time has come for law firms (and professional services firms more broadly) to realise that if we want to maximise revenue and, potentially, profit we need to rethink how we generate that revenue.

One alternative that the likes of Ron Baker and Mark Stiving have been banging the drum about for some time is ‘subscription based pricing’.

The benefits of adopting a subscription based pricing model

I have posted previously on this blog about the benefits of subscription based pricing (see here), but leaving all that aside for a second; as Amy Gallo wrote way back in October 2014 in the Harvard Business Review (see ‘The Value of Keeping the Right Customers‘) with the acquisition costs of acquiring new customers running being between 5 and 25 times more expensive than servicing existing customers, it makes economic and financial sense to find, and keep, the right customers.

How you price this is probably the most important step along that path.

The weakness of having billable hours as your default billing method is that you are pricing to the transaction. Whereas one of the greatest benefits of the subscription based pricing model – or even a retainer based pricing model if you must at the start- is that you start thinking about pricing the customer or even the portfolio.

In other words, you start to think about the customer and their needs first. And for an industry that always talks about the customer being at the centre of everything we do, doesn’t it makes sense that our pricing structure reflect this claim?

But it also makes sense internally, because it:

is smarter pricing

leads to smarter collaboration

moves you away from seasonal end of financial and calendar year pressures, and

helps remove any discussion around the ‘commodity’ tag.

Not to say, in these COVID-19 times, when you are talking working capital facilities with your bank, it provides you with a guaranteed annuity revenue stream.

Now who would not want that comfort right now?!

These just represent my thoughts though and always interested to hear your views.

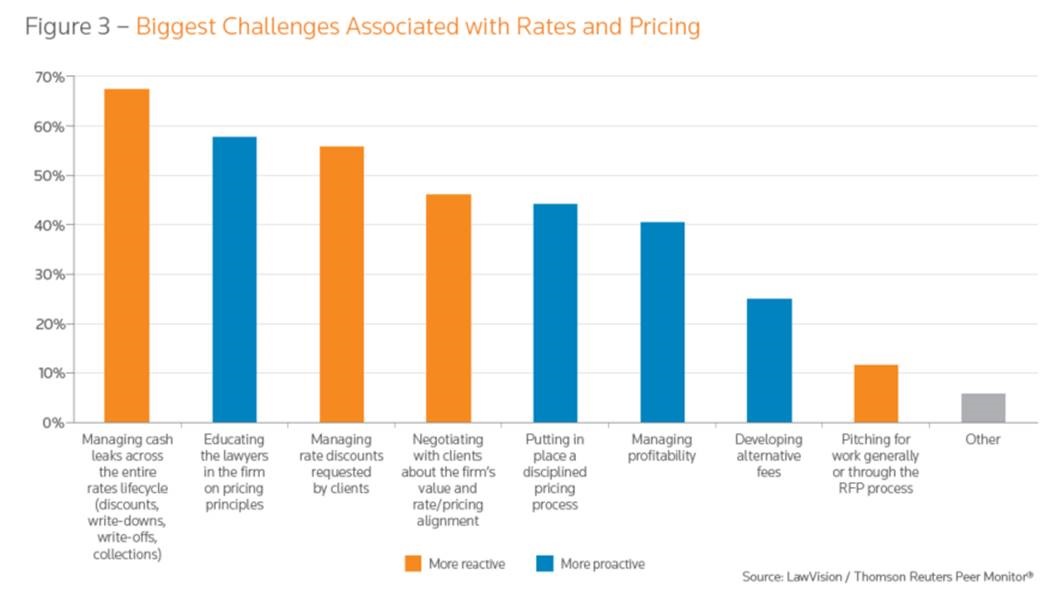

Predominately North American based, it’s nonetheless an interesting read – with some contentious stuff (see the ‘LawVision Maturity Curve’ for example) – for anyone even remotely interested in following the current trends and traits affecting law firm pricing issues. But what particularly grabbed my attention in this Report was the ‘8 biggest challenges law firms associate with rates and pricing’ (Figure 3):

And what really, really fascinated me about this list is how few of them actually have anything to do with either rates (if that’s the way you want to do things) or pricing.

As you can see from the list, in desending order they are:

Managing cash leaks across the entire rates lifecycle (discounts, writedowns, writeoffs, collections) – my comment: neither a rates issue nor a pricing issue, but a behavioural issue

Educating the lawyers in the firm on pricing principles – my comment: neither a rates issue nor a pricing issue, but a training issue

Managing rate discounts requested by clients – my comment: neither a rates issue nor a pricing issue, but a behavioural issue (and are we seriously still having this conversation!)

Negotiating with clients about the firm’s value and rate/pricing alignment

Putting in place a disciplined pricing process – my comment: neither a rates issue nor a pricing issue, but a training issue

Managing profitability – my comment: neither a rates issue nor a pricing issue, but an accounting issue

Developing alternative fees

Pitching for work generally or through the RFP process – my comment: can someone please let me know what this has to do with either rates or pricing!

Which leaves us with:

Negotiating with clients about the firm’s value and rate/pricing alignment, and

Developing alternative fees

Both of which, depending where in the buying cycle these conversations are taking place with your customer, could actually have something to do with a rates and pricing discussion.

But seriously, Challenges 4 & 7 of 8, and we wonder why law firms struggle with the concept of pricing and the disconnect between firm and customer.

And if we are really being honest and true to our clients, then even inward looking the #1 issue should not be ‘Managing cash leaks across the entire rates lifecycle (discounts, write¬downs, write-offs, collections)‘ but should rather be: ‘How are we rewarding and incentivising in our staff?‘ – because if the answer to that is ‘utilisation‘, then everything above is relatively meaningless.

As always though, interested in your thoughts/views/feedback.

Like many lawyers who have worked under billable hours or fixed fees, for most of my career I have pondered the question: “How can I make money while I’m asleep?”, or better yet, awake but not working!

Early in my career I thought I had the answer – subscription-based pricing.

At the time I was working with Linklaters on their Blue Flag program (see this article for an overview of what Blue Flag was all about) which essentially provided compliance related information to subscribers who paid a monthly fee. This was then extended to basic loan documentation that was created using automated software (an early version of HotDocs if I am not mistaken).

As I was to find out though, the problem with this business model is that there is always someone willing to undercut you on price, with little attention to the value you were providing.

And so I never really took it much further.

But I remained interested in the dilemma of how I, as a knowledge provider working on hourly or fixed fee arrangements, could make money while I slept (outside of writing a book and get loads of royalties).

A couple of things recently changed my view on this whole issue though.

That’s right, Apple – as of the date of writing this post – the world’s second biggest business by stock market value is moving towards a subscription-based business.

Which made me think – what’s the biggest doing?

Answer: ever heard of Amazon prime?

So if subscription-based pricing works for these big players, why not your law firm?

As always though, would be interested in your thoughts, views, feedback.