The size of your firm has no bearing on the amount you can charge clients.

Now if you have read the above quote and thought to yourself “of course the size of your firm has no bearing on the amount you can charge clients, clearly Smith has lost it again!“, then bear with me.

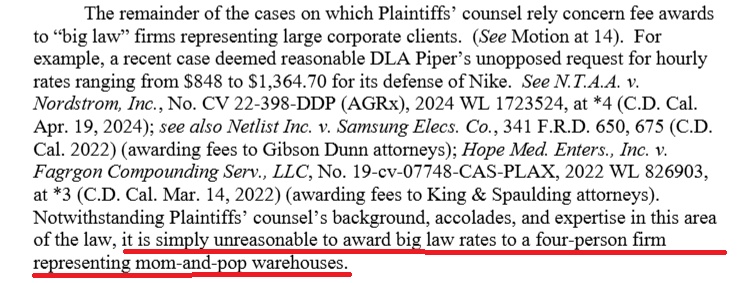

In a recent matter before the Central District of California, the Honorable Michael W Fitzgerald disagreed with the notion that the size of a law firm should have no bearing on the amount you can charge clients when he stated:

“it is simply unreasonable to award big law rates to a four-person firm representing mom-and-pop warehouses.”

In what is otherwise far reaching commentary on the history and application of the billable hour (well worth a read in itself), Fitzgerald’s ruling is troubling; not least because it is based on a premise that bigger means better — and better means more expensive. Now that could be true. But it doesn’t make it so.

Conversely, should I, as a client, be happy to pay more because the attorney acting on my matter works in a firm that has seven floors over one that has one? Surely the answer here is “no”, I’m paying for outcomes over inputs.

But that’s not the case here. If we follow Fitzgerald’s reasoning in this case, the real drivers of price: (a) Perceived expertise and relevance; (b) Client experience and accessibility; and (c) Outcome certainty and risk management, are certainly consideration, but no longer primary.

rws_01