Happy New Year and Welcome to 2019!

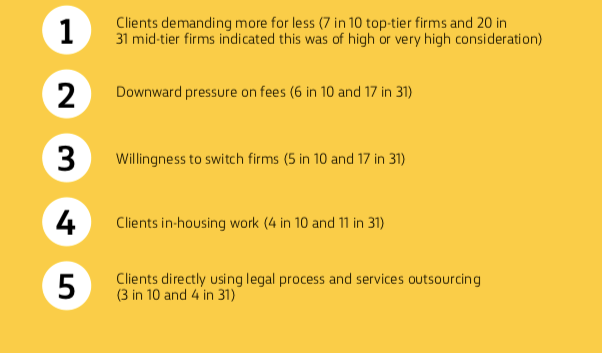

The recent (December 2018) Commonwealth Bank ‘Professional Services’ report highlights five challenges law firms in Australia are likely to experience further pressure on in 2019, which are:

- ‘Clients demanding more for less’

- ‘Downward pressure on fees’

- ‘Willingness to switch firms’

- ‘Clients in-housing work’

- ‘Clients directly using legal process and services outsourcing ‘

Each of these has it merits, while none is particularly new. So let’s take a quick look at each and assess them on their merit.

The call for ‘more for less’

It’s true, the call for ‘more for less’ continues. But I believe we may be misinterpreting the call a little here between what in-house really want (see Ann Klee, VP of Global Operations — Environment, Health & Safety, at General Electric Company – ‘less for less’) and what law firms believe they should be providing – a Rolls Royce service for a Toyota price tag.

My take: Neither client nor law firm are currently getting what they want and the net result is that nobody is happy with the relationship. Law firms need to get a better understanding of what is being asked of them. Scoping work properly – by experts – and then the subsequent professional project management of that is where the greatest return can come from here.

‘Downward pressure on fees’

Admission time!!:-

“I have never really understood the ‘downward pressure on fees’ argument”

Why?

Because, in order to be putting downward pressure on fees, surely you need to know upfront what that fee is – right?

However, if what you are saying is that this is actually a downward pressure on hourly rates argument, then I get where you are coming from.

But this is not the same thing as a downward pressure on fees argument, because there is little doubt in my mind that clients are willing to pay a premium on fees when the value of those fees have been fully explained and justified.

My take: despite the rhetoric, law firms still have a long way to go in understanding what in-house General Counsel are actually saying when they say “no surprises” on fee issues. And here’s a working reason why:- because while the GC can talk to legal issues the company faces, it’s the CFO who is responsible for explaining costs; and in more Australian companies than not, the GC reports to the CFO. A lesson in that for most private practice firms here.

A ‘Willingness to switch firms’

I often laugh when I see this one, because, really, ask yourself this: if most of your partners and lawyers are willing to switch to another firm, why shouldn’t your clients?

My take: if you want client stickiness, why not start with re-engaging with your own staff and get loyalty in your firm brand (something that hasn’t really happened since 2008 in Oz). Because while attrition will never be zero, if you can get your own staff on board as brand advocates you may find it a lot easier to convince your clients to hang-around.

‘Client in-housing work’

Without a doubt the biggest change in my working life has been the increase in in-house practitioners. A career in-house is now a very viable option for someone leaving university, something that was never even thought of in my day!

My take: the biggest competitors most law firms are not other law firms. It’s not even the #Big4. Don’t get me wrong, these are competitors, but nothing compared to the CFO of your major client working out its cheaper to hire a new lawyer in-house than pay your fees (see here for more on my views on your in-house competitors).

‘Clients directly using legal process and services outsourcing’

Not 100% sure what is meant by ‘outsourcing’ here. If this includes ‘on-shoring’, then I agree it’s a real threat.

My take: law firms in Australia will face a number of challenges over the next 12 to 24 months. Outsourcing, on-shoring will be among them, but I’m not sure I give them the same weight as the Commonwealth Bank Report does.

Some of the other issues I believe law firms here need to be aware of include further consolidation of the market (it remains too big for such a small market), staff retention issues, profit squeezes, technology and process improvements (and how, through change management champions, these are being handled within law firms because currently we are failing badly).

And finally, some 750 words into this post, we can mention the “innovation” word 🙂 .

Anyhow, guess you get the gist of where I am going with these so best of luck for 2019!

As always, would be interested in your views.