Hot on the heels of a post I posted two weeks ago summarising three reports on the state of the legal market, the last week of August has seen the publication of a further three survey reports.

1. The US Survey Report

The first survey report (Surveys Find Mixed Demand, Moderate Pay for Corporate Counsel) is out of the USA and summarises the findings from a questionnaire sent to 1,300 chief legal officers (CLOs) of the Association of Corporate Counsel (ACC) – who now have a Chapter in Australia.

This ACC survey covered wide ground, including pay rises (3%) and areas of in-house recruiting growth (compliance, contracts and corporate generalists), but probably my favourite take-out was the following two paragraphs:

“Organizations are looking for corporate counsel who can facilitate the business process, according to Peters. Counsel should become familiar with what the company does, take an interest and act as a support, instead of simply focusing on the legalities of whatever is presented to them, she said.

For example, corporate counsel might tour the company’s plant and observe the manufacturing process to better understand how the company works, according to Peters. This might allow the lawyer to help get the product to market quicker. “It behooves the lawyer to be involved and become an integral part of the company. Partnering with the business, you add and keep value,” she said.”

Private practice lawyers could move a lot further along the trusted advisor paradigm just by following that piece of advice.

2. The UK Survey Report

The second survey report (Mind the Gap: GCs, Firms Wide Apart in Perception) is actually a one-page infographic [downloadable here] done by the team at Briefing Magazine in the UK and provides further evidence, if ever we needed it, that there is a growing ‘value gap’ in the perception of the relationship between in-house counsel and their outside law firms & law firm managers.

This survey polled 125 GCs, 67% from companies with more than £1.1 Billion in revenue a year and more than 1000 employees, along with 86 managers (NB: Briefing Magazine‘s target readership is law firm leaders and managers) from the top 120 law firms in the UK.

Two take-outs from this survey of note are:

- on whether the process of buying legal services had moved to the in-house legal team’s procurement department, 80% of in-house GCs said they – and not the procurement department – had the say on who to send legal work to, whereas almost three quarters (74%) of law firms said exactly the opposite (ie, procurement had the say here).

- on the issue of AFAs (alternative fee arrangements), 76% of law firms believe that in-house GCs want to move away from the billable hour, whereas only 58% of GCs said they do.

Interesting as they are, both of these responses really highlight to me that most law firms out there are not having proper conversations with their clients around how legal services are being procured and, importantly, paid for.

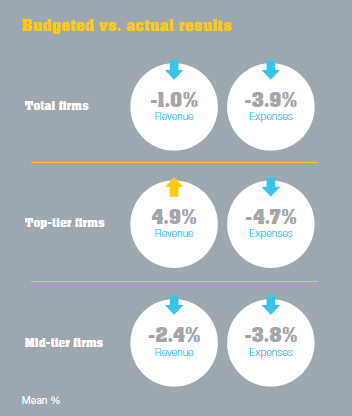

3. The Australian Survey Report

The third survey report of the week was the most comprehensive.

Authored by Joel Barolsky and published by The Melbourne Law School and Thomson Reuters Peer Monitor, the 2015 Australia: State of the Legal Market report sets out the dominant trends impacting the Australian legal market in 2015 and the key issues likely to influence the market in 2016 and beyond [a copy of which is downloadable here].

As you would imagine, a survey report of this nature (15 pages) packs a punch and there are way too many take-outs to summarises them all here so if you are interested in the finding of this report, but don’t have the time to read the whole thing, I would like to suggest you take a look at Joel’s post on LinkedIn – Key takeouts from major new legal market report – summarising the findings.

For me, it was interesting to see the survey confirm a trend I identified last year in the market, namely that the biggest competition private practising lawyers have these days is actually in-house counsel. I think this is further evidence that private practice lawyers are not doing enough to explain to their in-house counsel the benefits of using outside counsel.

In short, to my mind the conversation should not simply be: “I’m spending $150,000 on external legal each year, I can hire a lawyer and bring this work in-house“. Although I very much fear that is exactly the conversation that is taking place. And when you keep in mind that the two principal areas of concern for in-house counsel are compliance and risk, you’d think this provides external legal with exactly the right platform to have the conversation around why taking work in-house should not be a growing trend.