The end of November saw Legal Week (legalweek.com) putting on the second of its Asia regional ‘Corporate Counsel Forum’ events in the Gallery Room of Singapore’s Grand Hyatt hotel. Judging by the impressive collection of 220 regional in-house lawyers who attended, this event is likely now a firm fixture in the diaries of many in the industry. And rightly so. Events of this calibre are few and far between and should not only be welcomed, but encouraged.

Legal Week’s Elizabeth Broomhall wrote up a very succinct account of what took place at the Forum in a post on the Legal Week website on 5 December [2014].

In summarising the day’s events, and following subsequent discussions with Lucy Siebert, international counsel at Australia’s Telstra, and Julia Shtepa, managing director of legal for South Asia at Accenture, Elizabeth’s article highlights the following 5 issues (among more) as issues in-house team in the region have identified as being important to them when selecting outside counsel.

1. Local or International?

It would appear that in-house counsel in Asia are not immune to a discussion that is taking place on a more global level; namely:- should we be hiring local or international law firms?

On the one hand, there are many benefits to hiring an international law firm to act on your matters. On the other, particularly in the mixed legal landscape of Asia (where common and civil law sit side-by-side), there really is no substitute for – as Siebert calls it – “on the ground knowledge”.

I would wholeheartedly agree that there are complex issues in play here, as it is indisputable that there are very clever lawyers working with leading country and regional law firms. That’s why I was particularly drawn to Shtepa’s comment that:

“Sometimes Accenture will engage an international firm to play a ‘deal coaching’ role, she said. “Depending on the regulatory environment and the language constraints, it may be that the deal is led by an international firm and supported by a local firm”.”

If you can afford it, then this seems to me to be a very clever approach to take.

Alternatively, a case could be made that in-house counsel in Asia, as is the case in other parts of the world, look to instruct the lawyer and not the law firm.

2. Panel or no panel?

Client legal panel arrangements are the bane of many a private practice lawyer and their marketing team. Many an hour is spent responding to these and Australia, the home of Telstra, has undoubtedly played a major role in the development of this arrangement. Indeed, many of the ASX 200 have both Australia and Asia legal panels in place. So I was surprised to see Broomhall write that:

“many regional counsel believe these [panels] remain difficult in Asia given the limited capacity foreign law firms have compared with in their home markets, the different practice restrictions on foreign law firms across jurisdictions, the high turnover of partners in the region and the fluidity of the markets.”

While each of these is valid in their own right, none are unique to the region – and certainly would not seem to me to be an impediment to implementing a panel arrangement if the desire was there to do so. No, I would contend that there are two additional factors that mean panel arrangements are not, yet, as prevalent in Asia, which are: (1) relationships still trump all when assigning work; and (2) the rise of procurement is still to come.

That said, as Broomhall herself says: “An increasing number of companies, including Chinese state-owned organisations, have been moving in this direction in a bid to control costs” – and given the number of tender writing jobs that require local/regional language skills (notably Mandarin) that I have seen advertised in the last 3 months, my guess is that this [implementing panel arrangements] will be one of the major growth areas in 2015. Indeed, I will be interested to see what the position on this issue is at the Forum in 2015!

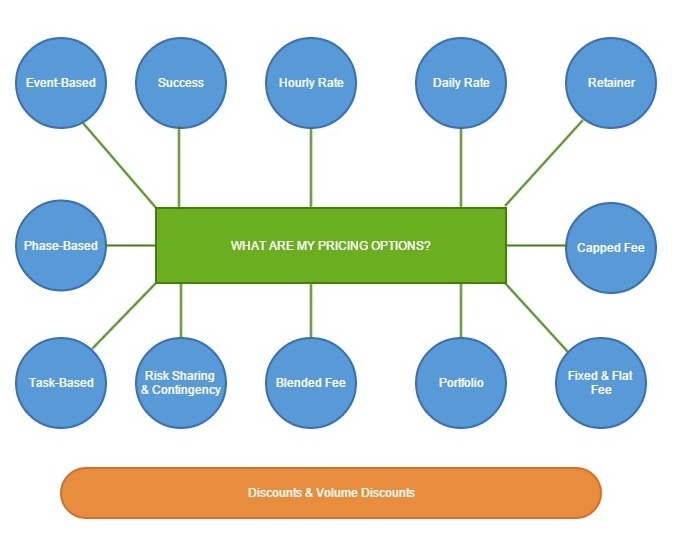

3. Where are all the Alternative Fee Arrangements (AFAs)?

Throughout my time in Asia, law firms have had to be very conscious of their cost-base as clients have always been value drivers. And with annual ROI profit margins of around 20% (which translates to probably the lowest ROI returns in the industry globally), many would say rightly so.

Leaving this aside however, I found myself in total agreement with the comment that when it comes to innovative fee arrangements, Asia lags behind the West.

Actually, with my interest having been spiked in this issue I went online to try and see how many firms had ‘on the ground’ regional Pricing Directors (a role that has seen phenomenal growth in both Europe and America, and less so here in Australia) and I couldn’t find one law firm that had an on the ground head of pricing present in the region.

All of which screams: law firms who can create opportunities to genuinely discuss the value exchange and AFAs with their clients have a massive opportunity to differentiate themselves in what is currently an extremely tight market.

4. Secondments and other value adds

It was interesting to note that both Siebert and Shtepa agreed that “secondments are also an opportunity to add value”.

In my experience, the staffing structure of law firms in Asia – which need to necessarily be tight because of the control on costs – has, historically, not leant itself to law firms offering secondments to corporate clients (historically, as part of a global offering, financial institutions have tended to fair better here).

Clearly, going forward, one of two things will happen: either law firms will need to revisit this discussion, or New Law providers –such as Lawyers on Demand and Riverview Law – are going to find a very nice gap in the market – indeed, many may argue that Advent is already taking advantage of this exact situation.

And law firms who doubt this should note Siebert and Shtepa’s comment that:

“secondments help lawyers in private practice gain a better understanding of their businesses. Indeed, they believe this is the key overall message to get out to firms: get to know our business; understand our drivers.”

and one of the best ways to do that – a secondment.

5. A more diverse profession

I wanted to finish this post on what I consider to be an important note of hope from Siebert’s comment that:

“We [Telstra] specifically look to see that they’re ensuring the best possible talent pool for us – not just white Anglo-Saxon males. We’ve got a very strong diversity policy and so we expect that to be something that is also important to our panel firms.”

If you haven’t already read Elizabeth’s article, I would like to strongly recommend that you wander on over there now…