Last week the Center on Ethics and the Legal Profession at the Georgetown University Law Center and Thomson Reuters Legal Executive Institute and Peer Monitor published their ‘2020 Report on the State of the Legal Market‘. This annual Report sets out the publishers’ views of the dominant trends impacting the legal market in the United States in 2019 and the key issues likely to influence the market in 2020 and beyond.

The Introduction of this year’s Report looks at ‘Incremental Improvement vs. Radical Change‘, as it might apply to the current state of the legal industry.

Drawing on the story of Dick Fosbury’s performance at the Mexico City Olympics in 1968, at which Fosbury stunned the world by setting a new Olympic record in the men’s high-jump event using a technique (the Fosbury flop) that had never been used in competition anywhere else previously, the Introduction to this year’s Report sets a great – and somewhat dramatic – backdrop to what it considers constitutes radical change against incremental change.

The Fosbury flop, without doubt, was radical change to a long held practice in 1968. But, post 1976, when all three medallist used the technique, it can also claim to be the victim of incremental improvement/change, as there hasn’t really been any great leap forward in high jump technique since.

So what has this all to do with the legal industry?

Well, it’s like this, probably since the mid-1980s the legal industry has undergone a series of incremental improvements, without really being the subject of any radical change. But, as the Report eludes, the last 12 to 18 months in the legal industry may have seen a shift here. The re-emergence of the Big 4, growth of legal tech, alternative legal service providers suggest a cusp of radical change is on the horizon (if it hasn’t already arrived).

So has it?

Well, I’m not so sure. Let’s take a look at some of the graphics in the report:

The graphic above looks at leverage of lawyers in US firms. Aside from the ‘Midsize’ firms, where a type of diamond is forming, the AM Law 100 and 200 look like very traditional law firm pyramids to me.

This second graph looks numbers of hours worked per lawyer and this looks to have flat-lined since the GFC in 2008. So no real change there.

This second graph looks numbers of hours worked per lawyer and this looks to have flat-lined since the GFC in 2008. So no real change there.

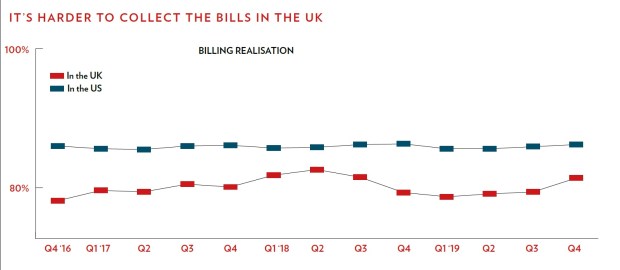

This third – and last – graphic looks at collection realization against agreed worked and, again, has pretty much flat-lined over the past 5 years at a relatively horrid 89.5%.

This third – and last – graphic looks at collection realization against agreed worked and, again, has pretty much flat-lined over the past 5 years at a relatively horrid 89.5%.

Collectively these three graphics paint a rather sad story to me. There may be change in the industry. But it is far from radical. And one may argue it really hasn’t even been that incremental post 2008; with the caveat that you also need to be mindful that not all industry segments are now equal, as some are clearly more equal that others!

As always though, read the Report as I’d be interested in your thoughts/views/feedback.

rws_01