Has the death knell of #BigLaw been rung too early?

Despite all rhetoric to the contrary, three reports published within the past week would suggest that the business model of #BigLaw is far from dead.

1. Citi Private Bank’s Law Firm Group report*

The first, published in the American Lawyer, was Citi Private Bank’s Law Firm Group‘s quarterly report on financial performance in the legal industry.

While this report headlined as ‘Despite Growth, Law Firm Forecast Dims for 2015‘, it is worth noting the following three paragraphs from the report:

“Looking at the results by firm size, the Am Law 100 firms saw demand and revenue momentum build. For the Am Law 1-50, part of the positive momentum is due to some moderation in 2014 results from the first quarter to the first half. The Am Law 100 firms are also better poised than smaller firms for near-term revenue growth, given that they had comparably larger inventory increases (especially in accounts receivable) at the end of the second quarter.

The Second Hundred was the only segment that saw a drop in demand. It also had the lowest increase in inventory (2.3 percent), so the third quarter will likely be particularly challenging for these firms.

Despite the momentum generated by the largest firms, it was the niche/boutique firms that had the strongest first half overall. Revenue was up 7.0 percent on the strength of a shortened collection cycle (compared with a lengthening for the Am Law 100 and Second Hundred segments), as well as modest increases in demand and rates. The niche/boutique firms also posted the smallest increase in expenses, 1.9 percent, creating a substantial widening of the profit margin. Because of the accelerated inventory turnover and only modest improvement in demand, however, inventory for these firms was up only 2.8 percent. These smaller firms may therefore find the second half of the year more challenging than the first half.”

So, while mid-tier firms appear to see revenue in decline, the top-end of town was actually seeing demand and revenue momentum build.

[* The results of this report are based on a sample of 177 firms (83 Am Law 100 firms, 45 Second Hundred firms and 49 niche/boutique firms)]

2. BTI Consulting report**

The second report is a snippet from BTI’s Annual Survey of General Counsel and goes under the bye-line: ‘Large Law Edges Out Mid-Sized Firms for New Work, with Higher Rates‘.

Here, BTI Consulting’s research found that:

“60% of law firm hires went to larger law firms (650 lawyers or more) in the last year. Clients report hiring large law as a result of increased and more pointed attention—think industry knowledge and more specific discussion of company issues. Think less about your firm statistics and more about the people to whom you are talking.”

Possibly more damning, however, was the observation that:

“The onus is on mid-sized firms to do better. Clients expect mid-sized firms to bring more client focus and more business understanding than large law—but are not always getting what they expect. And, mid‑sized firms have to demonstrate vastly better understanding of their potential clients’ targeted objectives than large law.”

[** Research is based on 280 in-depth interviews with corporate counsel at companies larger than $750 million in revenue as part of BTI’s ongoing Annual Survey of General Counsel.]

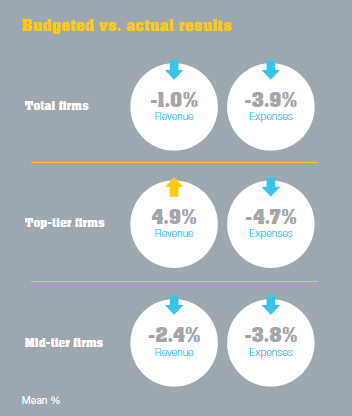

3. CommBank Legal Market Pulse Conducted by Beaton Research + Consulting

The last report is a little closer to home, Q4 2014 results from CommBank’s Legal Market Pulse conducted by Beaton Research + Consulting.

I’ll most likely review the findings of this report more closely in a post later this week – and it may even be interesting to compare them against previous Q2 & Q3 reports – but for the purposes of this post I believe we don’t really need to go past the following infographic from the report:

which would certainly seem to indicate that “top-tier” firms are far happier with overall FY2014 results than their “mid-tier” cousins.

Bringing it all together

So, what does this mean?

To my mind what these three reports cumulatively evidence is this:- while #NewLaw may have arrived, and while it may be here to stay, what is increasingly clear is that #BigLaw is not the market segment that needs to be concerned with this development.

Nope, dig a little deeper and I think you’ll find that it is actually Managing Partners in firms with revenue in the A$20-A$70 million range who will be having a lot more restless nights sleep…