Earlier today, the Thomson Reuters Institute published its Midyear Update on the Australian Legal Market, providing valuable half-year insights into industry trends in the Australian legal market.

There’s a lot to unpack in the Report, and I highly recommend you download it. That said, here are my top takeaways:

✅ What’s Happening with Non-Equity Partners? Is there an underlying story in the Non-Equity Partner segment? The data suggests there might be more to explore.

✅ Equity Partners Carrying the Load? If legal market demand and worked rates are up in 2024, yet the average billable hours per lawyer are down, it raises a big question—are Equity Partners absorbing the extra workload? If so, why?

✅ Billable Hours Decline With 12 months in a year, many law firms have lawyers billing less than 1,500 hours annually. What does this mean for profitability and productivity?

If you’re looking to refine your pricing strategy or need guidance on law firm profitability, feel free to get in touch. In the meantime, download the two-page update and see the data for yourself!

A recent article by BTI Consulting’s The Mad Clientist (‘Did Clients Just Go Sour on Rankings and Directories?’ published on 12 February 2025) states that:

Thought leadership now outweighs rankings – especially when forming new relationships.

While we talk often about “thought leadership” in professional services, I’m not entirely sure we understand the mechanics and actualities of what constitutes “thought leadership”.

For a start, if you say you’re a “thought leader” chances are you’re not – as only others can pin that tag on you!

So, I thought I would do quick run through what thought leadership means to me, as well as some ways you might be able to demonstrate your knowledge in such a way as others start to consider you a thought leader!

What is ‘Thought Leadership’?

Thought leadership is the art of positioning yourself, or your firm, as a leading authority in a particular area – industry or field – by sharing (typically for free) valuable insights, expertise, and innovative ideas.

Thought leaders influence their audience through content such as articles, blogs, speeches, books, research and social media engagement.

Key Aspects of Thought Leadership

Expertise & authority: Thought leaders have extensive knowledge in their field and are trusted sources of information.

Innovative thinking: Thought leaders challenge conventional wisdom and introduce new perspectives or solutions.

Content creation: Though leaders share insights through blogs, articles, whitepapers, podcasts, videos, or public speaking.

Engagement & influence: Thought leaders actively participate in discussions, mentor others and drive industry trends.

Authenticity & credibility: Genuine thought leaders prioritise value over self-promotion, building trust through consistency.

How can I display thought leadership?

Many professional firms limit their content strategy to publishing articles on their firm website and stopping there. While this is a good starting point, it doesn’t fully leverage the power of content marketing to attract, engage, and convert potential clients.

To expand your reach and establish your authority as a thought leader, consider adopting the following to your content marketing strategy:

Blog posts: Either via your own blog page or your firm’s (or even both), regularly provide in-depth insights, case studies, and industry updates. From time-to-time offer to guest post on other people’s blogs as well.

Newspaper comments and articles: Write a regular column in a reputable newspaper on your area of expertise. You can also become a source of commentary – newspapers are always seeking commentary from industry leaders.

Whitepapers & eBooks: Offer comprehensive research findings, legal guides, and thought leadership content. Look to position both yourself and/or your firm as the trusted authority in that area/field.

Videos: Create a YouTube or TikTok account and make videos that help explain intricate and complicated topics in a dynamic, accessible and easy to consume way.

Webinars & Live Streams: Host real-time discussions, Q&A sessions, and educational webinars – either on your website or via other platforms such as LinkedIn.

Podcasts: Either host your own podcast or provide expert insights on podcasts hosted by others.

Social Media posts: Engage in relevant discussions on platforms like LinkedIn, Instagram, Facebook and X.

Email Newsletters: Share valuable insights, firm updates, and case studies directly with subscribers via email providers such as MailChimp.

Bringing it all together

Thought leaders are recognised by others for their deep knowledge of a subject matter and so have the ability to shape conversations, influence decisions, and inspire others. These are all attributes that will help expand your audience reach and establish credibility in your area – leading to a higher number of requests for assistance and a bigger book of business!

Feel free to get in touch if you need help with your thought leadership strategy.

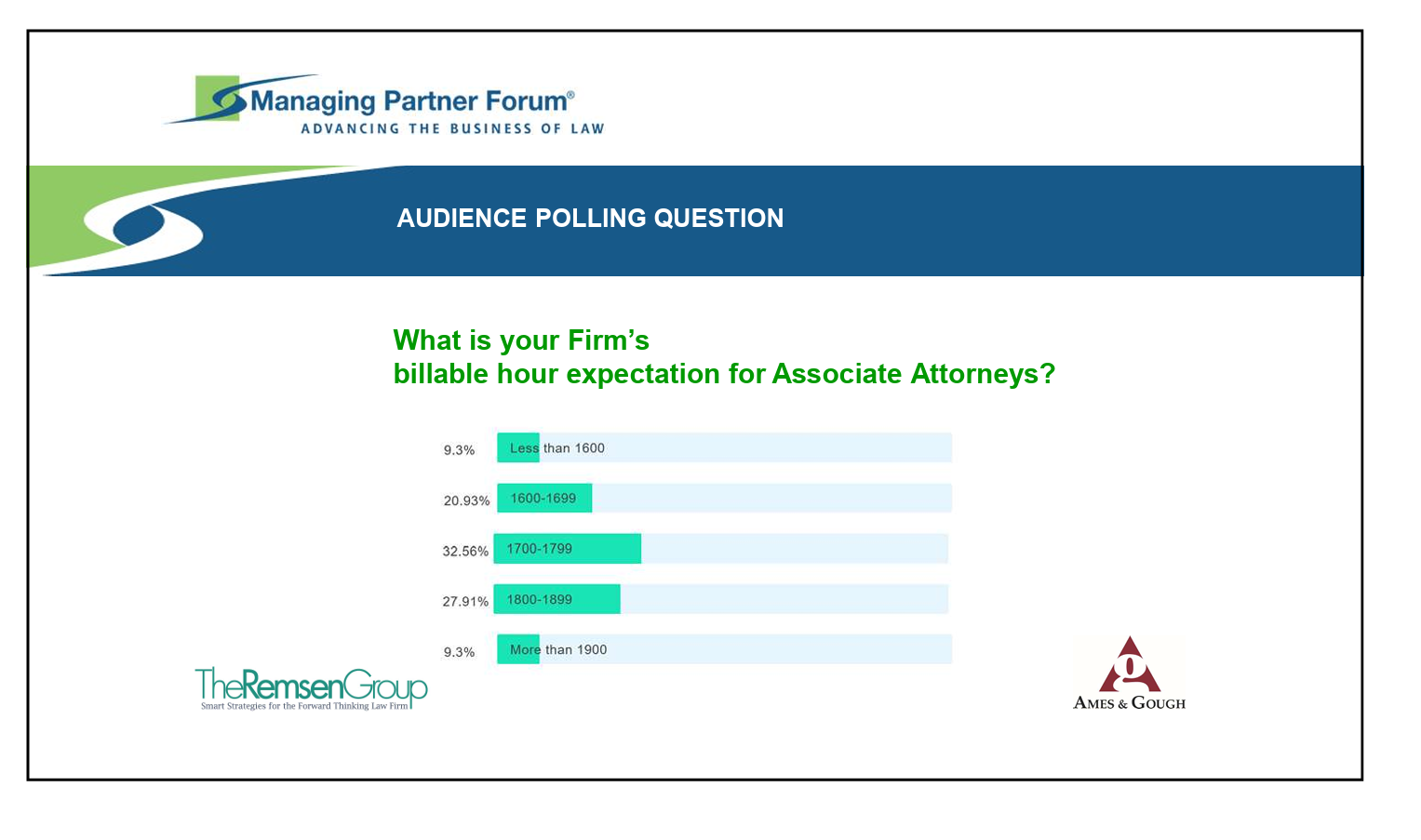

It’s interesting to note that nearly 70% of respondents expect their Associate Attorneys to bill over 1700 hours a year, with almost 10% expecting over 1900 billable hours per year.

That’s a lot of billable hours! And if we consider the ‘10-20-30-40 Leverage Rule‘, then the implication is very bleak for junior lawyers!

And as I say to those entering the legal profession who need some understanding of how many hours they need to work to meet their billable hour target, take a look at Yale Law School’s ‘The Truth About The Billable Hour‘.

While I am all for the profit motive, I maintain that if owners and managers of law firms want to understand why they have a high attrition / burnout rate in their teams, take a close look at what expecting someone to bill 1700 hours a year is actually doing to them!

Having just posted yesterday on ‘Directory and Award Submissions‘, I thought it was somewhat timely that the team at BTI Consulting published the results of a survey they have conducted with over 350 corporate counsel which showed:

Only 4% still find rankings valuable

18% like them but aren’t strongly influenced

33% are ambivalent

45% express outright disinterest

Some of the commentary is just brilliant, including this gem:

With limited resources, should our firm prioritize directory or award submissions?

An excellent question.

So good, I thought I would try and answer it in this week’s BD Tips post.

The Goal: Brand awareness

When it comes to gaining brand recognition and visibility – for your law firm and its partners/principals – two leading strategies are directory and award submissions. Both have their own unique benefits, so let’s take a look at each in turn:

1. Directory submissions

Legal directories are comprehensive listings of law firms and individual lawyers. They provide potential clients with information about legal service providers – including leading lawyers in practice areas and client reviews.

Benefits

Increased Brand Awareness: Being listed in a reputable legal directory – such as Chambers, Legal 500, IFLR 1000, WTR or IP Stars, can enhance your firm’s online presence and make it easier for potential clients to find you.

Client Feedback/Testimonials: Most directories have clients feedback/reviews comments. These can be used in Marketing material (such as bids and tenders / capability statements / on your website) to help build trust in your firm’s brand and attract new business.

Cons

Cost: Submissions to all legal directories take significant time and input from fee earners. This time is otherwise billable on client matters.

Time-consuming: Submitting to directories is a time-consuming project.

Long lead time: Thinking just because you’ve submitted to a directory today means you will be listed straight away is naïve. Getting listed in a directory takes time. Like most things, it needs a strategic approach!

2. Award Submissions

Legal awards recognize excellence in various aspects of legal practice. Awards can be given to individual lawyers, law firms, or specific practice areas based on criteria such as innovation, client service, and case outcomes.

Benefits

Prestige: Winning or being shortlisted for a legal award can significantly boost your firm’s and it’s partners reputation and prestige within an industry and beyond.

Marketing Opportunities: Awards can be used in Marketing materials, press releases, and social media to attract new clients and retain existing ones.

Networking Events: Award ceremonies provide opportunities for lawyers to network with industry peers, potential clients, and referral sources.

Cost: Generally, award submissions are cost effective.

Cons

Competition: The process can be highly competitive and there are no guarantees of winning!

But, which should we do?

The decision on whether to do a directory or award submission ultimately depends on your firm’s current brand awareness strategy and goals.

If your firm is looking to improve brand awareness, a legal directory submission might be the way to go.

On the other hand, if your firm’s primary goal is to boost your firm’s reputation and gain recognition within an industry in the short-term, legal award submission can be a much more beneficial tactic.

The fact is that both play a critical role in enabling your firm’s marketing and business development strategy by improving visibility, credibility, and client trust.

In a perfect world, you get to do both.

In an imperfect world: go awards for the short game, and directories for the long game!

As we start out on 2025, the 𝑨𝒖𝒔𝒕𝒓𝒂𝒍𝒊𝒂𝒏 𝑭𝒊𝒏𝒂𝒏𝒄𝒊𝒂𝒍 𝑹𝒆𝒗𝒊𝒆𝒘 (AFR) has helpfully published a table today (14.01.2025) – ‘𝐁𝐢𝐥𝐥𝐚𝐛𝐥𝐞 𝐡𝐨𝐮𝐫𝐬 𝐭𝐚𝐫𝐠𝐞𝐭𝐬 𝐟𝐨𝐫 𝐟𝐢𝐫𝐬𝐭-𝐲𝐞𝐚𝐫 𝐥𝐚𝐰𝐲𝐞𝐫𝐬 𝐚𝐭 𝐬𝐞𝐥𝐞𝐜𝐭𝐞𝐝 𝐥𝐚𝐰 𝐟𝐢𝐫𝐦𝐬’ – that makes for very interesting reading.

Other than the expected billable hour targets for first year lawyers and comments on alleged “under-billing” practices at major Australian law firms, what caught my attention in the article was this comment:

I might be wrong, but in the event that Hamilton Locke charges clients by the billable hour, then I highly suspect this also translates into a yearly hourly target…

…In the event that HL charges clients fixed fees or some other type of fee arrangement, then I accept this calculation probably sets it apart.

“…over the last two years the number of Am Law 100 lawyers based in Beijing and Shanghai has declined by 25% from 569 to 424. The decline over a five-year period is 35%.”

Over the past 12 months, Chinese Law Firms DeHeng, JunHe, Fangda Partners and Han Kun Law Offices have established overseas offices in Singapore, the U.S., Indonesia, South Korea, Vietnam, and the Middle East

Having worked with law firms around the world for close to 30 years to help establish their overseas offices (with a particular focus on Asia), I’m not sure I have ever seen such a significant shift in an in-bound/out-bound referral strategy.

In my view, we are now at the dawn of an era when Asian-based law firms are referring more work out of Asia than International law firms are referring work into Asia.

The only question that remains then is this: “How are you positioning your firm/practice to benefit from this shift?“.

When I was younger, my mother would often say to me: “Because it’s important to you Richard, doesn’t make it important to me“.

My mother had worked with lawyers earlier in her career, and I thought this piece of advice just profound (as you typically do with tidbits your mum says when growing up!). Until one day I was working with a partner who said exactly the same thing to me when I mentioned I had been waiting to see him all day!

So what’s the point I’m trying to make here?

Well, as with most things in life, when we think about what our clients need/want we think of this from the prospective of what we can provide them, rather what their true needs/wants are. To try and minimise this, I often ask my clients: “So What?“.

Asking “So What?” can sound abrasive. But, what it does is help to clarify the message, the reason, the rational we are sending to our clients about why they need our services/products and why they need them now.

And so I thought I would run through a high-level overview of the “So What?” test.

What is the “So What?” Test?

Being required to answer the “So What?” question is a means of evaluating the relevance and impact of your proposal/messaging to clients or prospective clients.

Answering this simple question demands clarity, purpose, and a focus on client outcomes – and helps move the narrative away from the product/service you are trying to sell.

If you are unable to answer this simple question convincingly, then your proposal almost certainly lacks relevance to the client and will not resonate with them.

Benefits of getting the right answer(s) to the “So What?” Test

Aligns your offer with the what the customer values

Asking the “So What?” question forces you to examine whether your solutions genuinely solve the customer’s problem(s). This alignment ensures you focus on outcomes that genuinely matter to your client.

Sharpens your messaging

In proposals and presentations, cluttered messaging dilutes impact. The “So What?” question helps eliminate unnecessary fluff and refines your message to its core purpose. Clear, concise messaging drives client engagement.

Helps build credibility

Proactively applying the “So What?” question puts you in the shoes of your client. You are able to anticipate their questions and build a solid case for your services/products. Demonstrating this level of critical thinking goes along way to establishing trust and credibility – it’s not about you, it’s about them!

Ultimately it saves you time!

Actively applying the “So What?” question acts as a filter to identify opportunities that are worth pursuing. If you can’t articulate why an initiative matters, it might not be worth the investment of time and resources pursuing that opportunity!

Bringing it all together…

The “So What?” test isn’t just a question – it’s a discipline. Asking the question allows you the opportunity to refine your message – to sharpen your focus, align your efforts, and ensure you’re solving the right problem, for the right person, with the right tools.

Incorporating the “So What?” test into your business development efforts will result in your business development activities becoming more impactful; your messaging more persuasive; and your win/loss ratio becoming more transformative!

As always, get in touch if you need help with your business development strategy and activities.

There are few more personal ways to thank a person for the support they have shown you and your business over the past 12 month than to send them a handwritten Christmas card.

Unlike e-cards, which to be honest I have never been a massive fan of (but can see both the financial and ecological savings if you are sending several hundred/thousand), a handwritten note in a Christmas card adds that personal touch to the message that, to me, enhances the gratitude being shown.

Some tips

If you’re going to send a handwritten note in a Christmas card to a key contact or referrer this year, make sure to:

Provide context: to why the card is being sent. For example: “it been a pleasure working with you over the past 12 months and we look forward to supporting you in the future”.

Personalise it: include a private note about something that happened this year.

Keep it professional: remember, it’s a Christmas card to a client/referrer, so be personal but keep it professional – no saucy joke cards you can find in some stores please!

Keep it brief: again, it’s professional, so keep it brief. The recipient of the card doesn’t have a lot of time to read this card and probably has a few more cards than just yours to read, so make sure to keep this to a couple of well-thought-out sentences at most.

The simple, relatively inexpensive, gesture of sending a handwritten Christmas card can leave a lasting impression on your client. It could well be the small differentiator that you are looking for to stand your business out from its competitors in 2025!

As always, get in touch if you need help with your business development strategy and activities.