Earlier today, the Thomson Reuters Institute published its Midyear Update on the Australian Legal Market, providing valuable half-year insights into industry trends in the Australian legal market.

There’s a lot to unpack in the Report, and I highly recommend you download it. That said, here are my top takeaways:

✅ What’s Happening with Non-Equity Partners? Is there an underlying story in the Non-Equity Partner segment? The data suggests there might be more to explore.

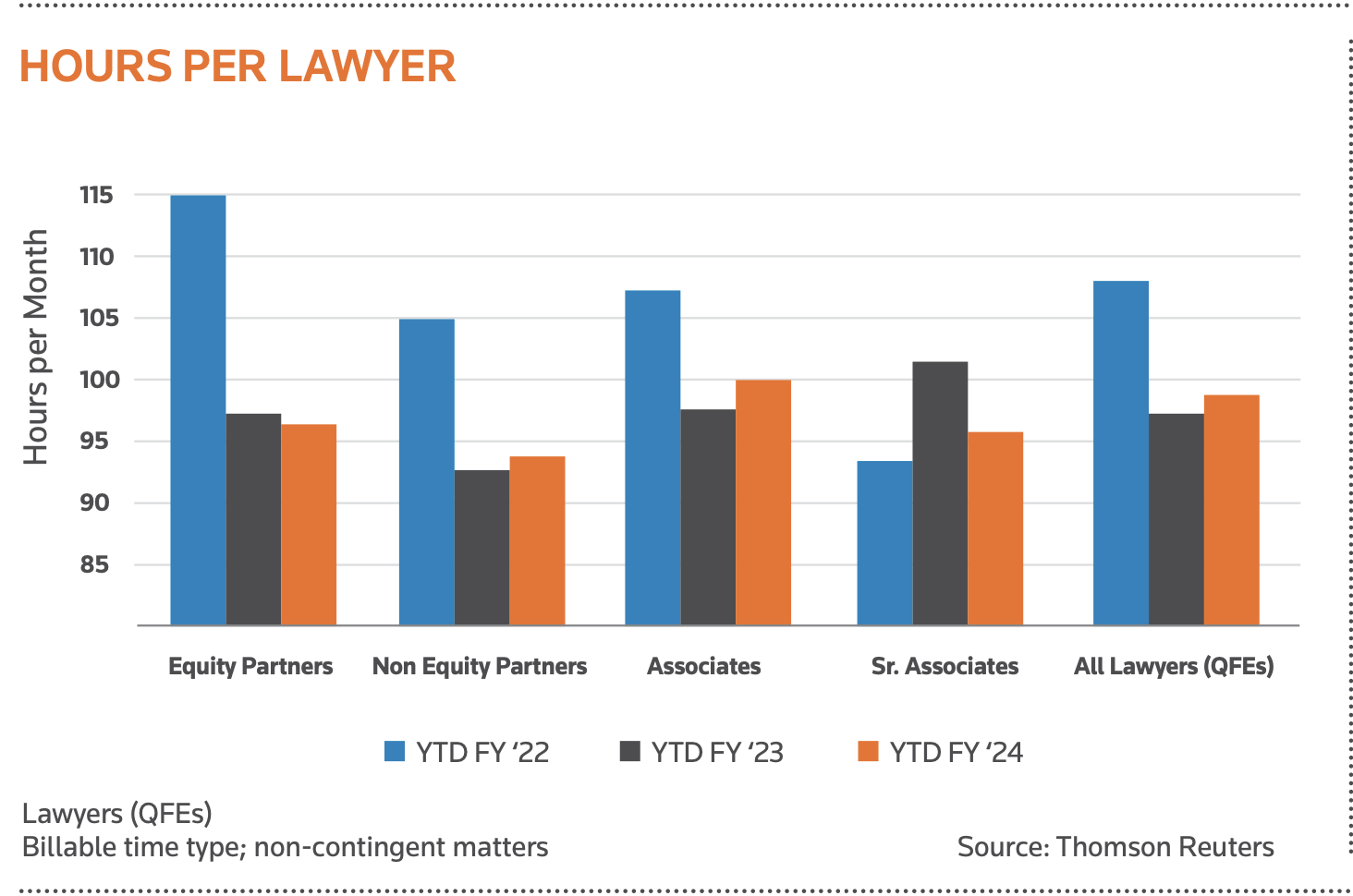

✅ Equity Partners Carrying the Load? If legal market demand and worked rates are up in 2024, yet the average billable hours per lawyer are down, it raises a big question—are Equity Partners absorbing the extra workload? If so, why?

✅ Billable Hours Decline With 12 months in a year, many law firms have lawyers billing less than 1,500 hours annually. What does this mean for profitability and productivity?

If you’re looking to refine your pricing strategy or need guidance on law firm profitability, feel free to get in touch. In the meantime, download the two-page update and see the data for yourself!

A measure of total billable hours worked by the average law firm

Leaving aside the flaws in that definition, if we are to use it as a yardstick for year-on-year growth and a like-for-like comparison globally, then the Australian legal sector looks positively healthy – particularly so for those practising Dispute Resolution (9.5% growth year-on-year, although I question the low starting bar here as DR has suffered a number of negative years as a result of COVID) and “General” Commercial (7.5% growth year-on-year; and while no definition of “general” is provided it clearly doesn’t include M&A, which sits in a different bucket).

Black clouds? If there is a black cloud around the numbers it’s leverage and expenses.

As the chart above indicates, leverage between partners, senior associates, associates and lawyers still looks out of shape when compared against firms in other jurisdictions.

What this chart indicates to me is that partners (in particular, equity partners) are still doing way too much of the billable work and not pushing the work down to more junior lawyers (which might be understandable if it was salary partners looking to make equity; but kind of suggests it is equity partners looking to retain equity points – maybe a post for another day!).

Having said this, it might also be a trait of the Australian legal market. We often don’t follow the 10-20-30-40 leverage model here in Australia.

A potential second black cloud is on the expense-side: lawyer renumeration.

While this appears to have cooled – down from 13% growth in 2023 to 7.3% growth in the first half of 2024, for those of us who work in this market day-in, day-out, there is an acknowledgement and acceptance that mid-level lawyers (those between 4 and 8 years PQE) are rare as hen’s teeth.

And the reason for that is simple – most see Australia as a small fish bowl and want to spread their wings in Asia, London or New York.

Who could blame them!

Some come back, many don’t.

But what it does mean is this: we pay a premium for mid-level [good] lawyers here in Australia!

The last black cloud has to be lateral partner movement.

The Thomson Reuters midyear market update doesn’t include a section on lateral partner movement, but it should. Not only because it would make for interesting reading, but also because it’s a good indicator figure.

As always, get in touch if you want to talk through any of the above.

Law firms that conduct formal client feedback programs can earn nearly twice the share of a client’s external legal spend than a firm not engaging in feedback;

in 2023, only 27% of clients were asked to participate in a client feedback program by their outside law firms.

Let’s get a realty check on that: Law firms that have a client experience (CX) feedback program can earn nearly twice the share of a client’s wallet, but less than one in three clients have been asked to participate in a client feedback program.

In business development we often talk about “low hanging fruit” and this seems like a ‘no brainer’ to me!

Get in touch if this is something that interests you. And, frankly, why should it not!

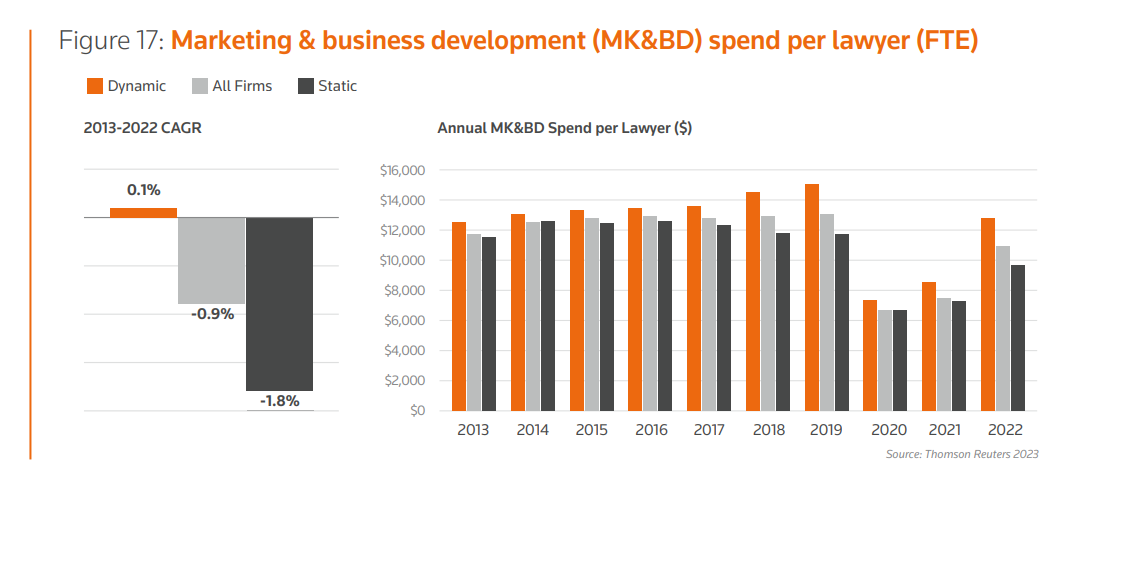

The numbers have been crunched and the results are in: ‘Dynamic Law Firms’ invest considerably more in their business development and marketing activities/departments than static firms are willing to do.

According to the latest (8th) iteration of Thomson Reuters Institute’s 2023 Dynamic Law Firms Report, Dynamic Law Firms consistently invest greater sums in their business development and marketing teams than Static Law Firms:

As you can see from the over graph, in 2022, on average, this investment by Dynamic Law Firms in their business development and marketing teams accounted to over $12,000 per lawyer. Roughly $2,500 more per lawyer than Static Law Firms.

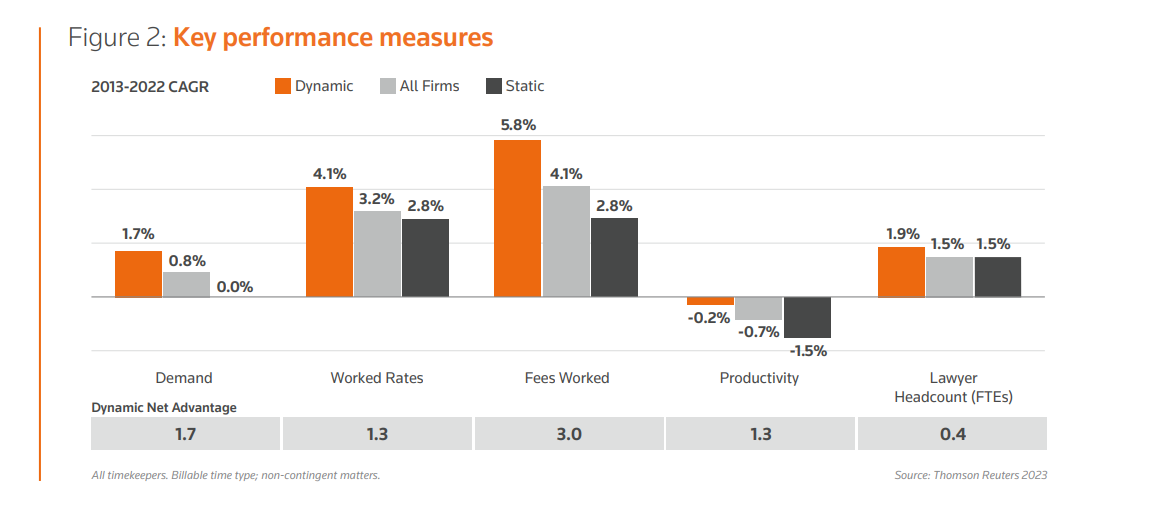

Importantly, this investment in business development pays off:

With Dynamic Law Firms consistently outpacing Static Firms in all growth Key Performance Measures; but, most notably from a business development perspective, in both ‘worked rates’ and ‘fees worked’.

So why is this? After all, business development and marketing is a ‘cost-center’.

Well, as the Report itself states:

“The first goal of MK&BD investment is to raise top-of-mind awareness of the law firm.

Research conducted over the course of many years by the Thomson Reuters Institute has shown that top-of-mind awareness is a vital first step toward winning work – a process that will see a firm move along a continuum from awareness to being viewed favourably, to being considered for and ultimately winning work, and hopefully, to a point where the firm has gained enough experience with the client that they garner credibility in the board room and can begin to box out competitors.”

A fact backed-up by the authors of Simple Heuristics who, in their principle of “recognition” [firm brand or lawyer], state that recognition is number one in any client’s decision process around whether or not to buy something.

And so it goes without saying that this ‘awareness‘ factor is critical in the ‘buying cycle’. If we don’t have this advantage, then we need to hope to hell the other providers aren’t a known commodity so we can proceed to the next level in the buyer’s decision process (typically experience – have they done this before?; then can I trust them not to mess this up and make me look stupid! – SIDE NOTE: price isn’t in the top 3 decision making selection criteria.).

Which is why, if you want to make sure your firm stays one step ahead of its competition, you actually need to be investing more, not less, in your business development team right now.

Yep, the evidence is in. It’s undisputed. Business Development and Marketing is not a ‘cost center’ (not that I ever thought it was). They not only pay for themselves, but they ensure your firms stays ahead of its competitors and earns more $$$s.

So the next time you think to yourself: “I need to cut costs, I’ll cut my business development and marketing budget” – I’m here to tell you that’s dumb – think again, because not only will it hurt you but it will take you on a journey to blandness.

As always, feel free to reach out to me for a chat if you want to talk through how I can help with this.