In the 1994 movie of the same name, Forrest Gump is asked:

“are you stupid or something?”

to which Forest replies:

“stupid is as stupid does”.

Some 20 years later (yes, it really has been that long!), in general parlance this phrase has come to mean that:

‘an intelligent person who does stupid things is still stupid’ – (Urban dictionary)

and I have to say that this thought went through my mind earlier this week when I read that a third of [UK] commercial firms are likely to raise their rates in a bid to boost their profits (Solicitors Journal 6 May 2015 – “Number of law firms planning to raise charge out rates increases“).

Leaving aside the issue of whether a direct raise in your rates will equate to increased profits (for example, the psychological impact of rising rates/budgets on fee earners with no increased salary (cost)) – what in the world would make 26 (1/3rd) of so-called intelligent finance directors of the UK’s Top 100 law firms say “it is likely their firms will increase their charge out rates in order to improve profitability in the year ahead“?

As I have blogged countless times before (the most popular being: ‘Is it time for law firms to break with the RULES when looking at profitability?‘), hourly rates are but one of the metrics in calculating profitability. And it’s probably not even the biggest metric driving your firm’s partner profit levels, which almost certainly would be better achieved via an increase in your realised rate.

Putting this mathematically (admittedly not my strongest area), say my hourly rate is $100 and my realization rate is 90%, then I’m being paid $90-. Taking this forward I’ve decided to increase my hourly charge-out rate to $110-, but find that my realization rate has now fallen to 80%. If my maths is correct, I’m now being paid $88-.

In other words, in real terms, I’m losing money!

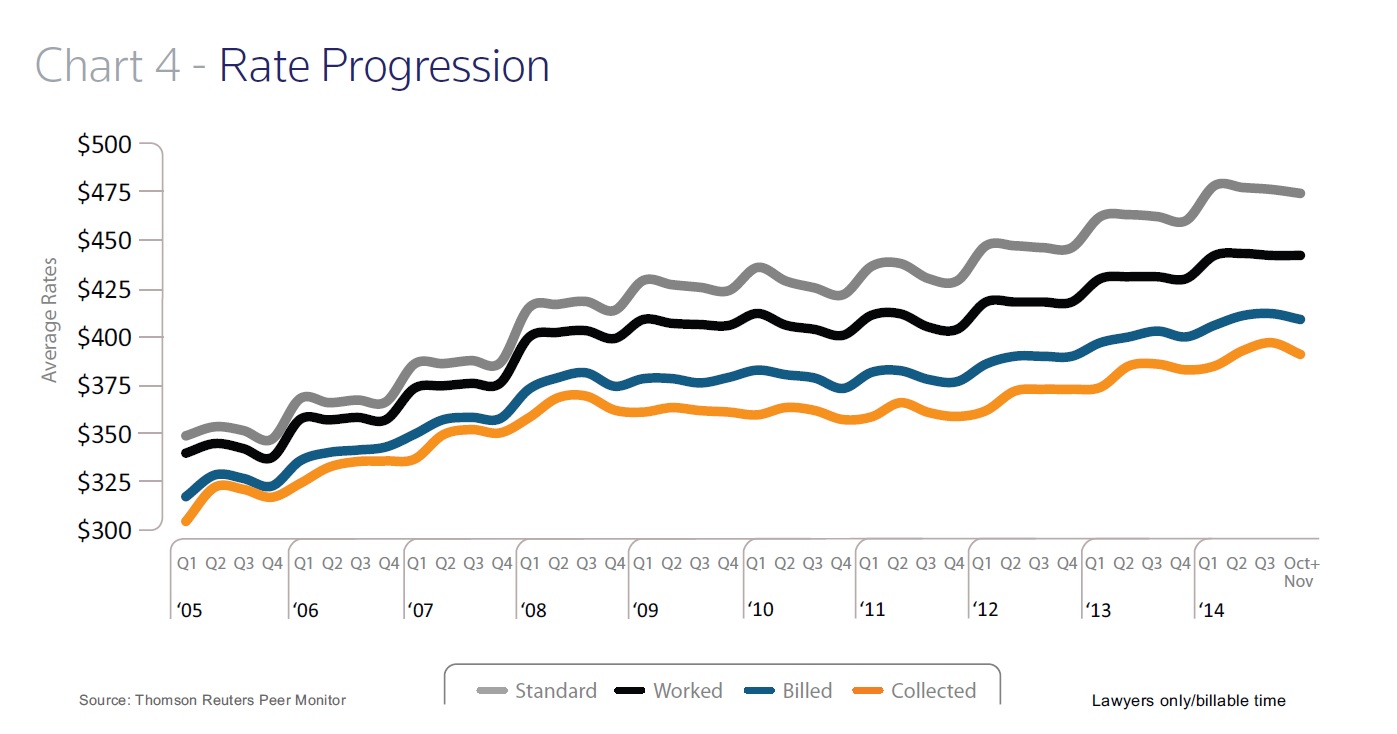

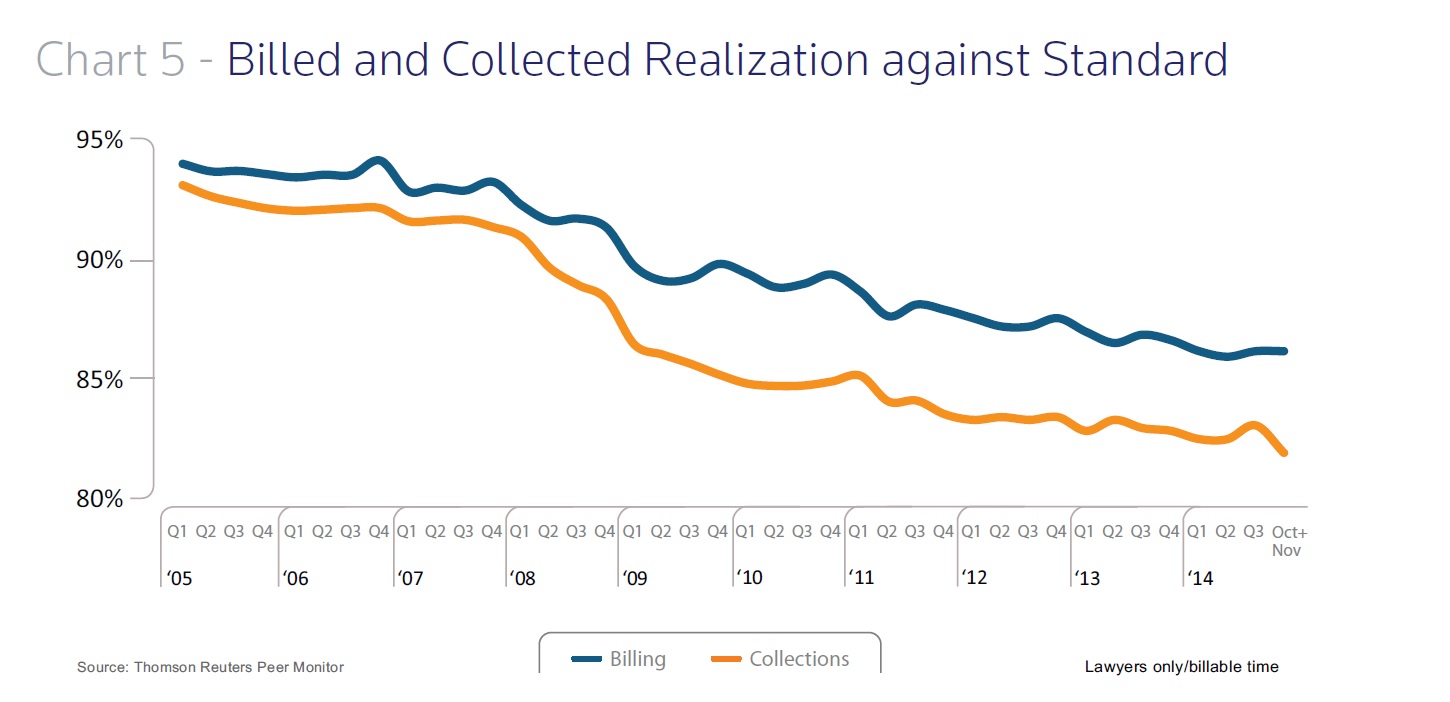

Don’t think this could happen? Then take a look at Charts 4 & 5 from the ‘2015 Report on the State of the Legal Market‘ published by The Center for the Study of the Legal Profession at the Georgetown University Law Center and Thomson Reuters Peer Monitor (at page 5)

Those charts don’t make for pretty reading.

So when, as the article reports:

“…firms realise this is not going to be an easy sell to clients who are likely to negotiate hard to keep fees down, so their approach to increasing charge out rates is likely to be softly softly, rather than gung-ho”

my response would be: “why bother?”.

Instead,

- try keeping your charge-out rate the same over the next 12 months;

- try not to give discounts;

- try to increase your realisation rate (by 3 to 5 cents in the dollar);

- try to reduce your lock-up days;

and see where you end up.

You may just find that has a better impact on your partner profitability numbers than the likely impact that is going to come your way when you go annoying and off-siding your clients with the almost obligatory 1 July 10% rate increase letter.

But I could be wrong…