My thanks to the team at Legal Practice Intelligence for publishing my thoughts on whether or nor Australian law firms have given up on their Asia dreams following the recent decoupling of King & Wood and Mallesons.

If you want to read the article, here is the link.

Earlier today The 𝘈𝘶𝘴𝘵𝘳𝘢𝘭𝘪𝘢𝘯 𝘍𝘪𝘯𝘢𝘯𝘤𝘪𝘢𝘭 𝘙𝘦𝘷𝘪𝘦𝘸 published the results of its Law Graduate Salary Range Survey.

Makes for an interesting read. On the one hand, nowhere near as high as overseas markets such as London, HK and the US. On the other hand, Grads on A$130K would have been unthinkable 5 – 10 years ago!

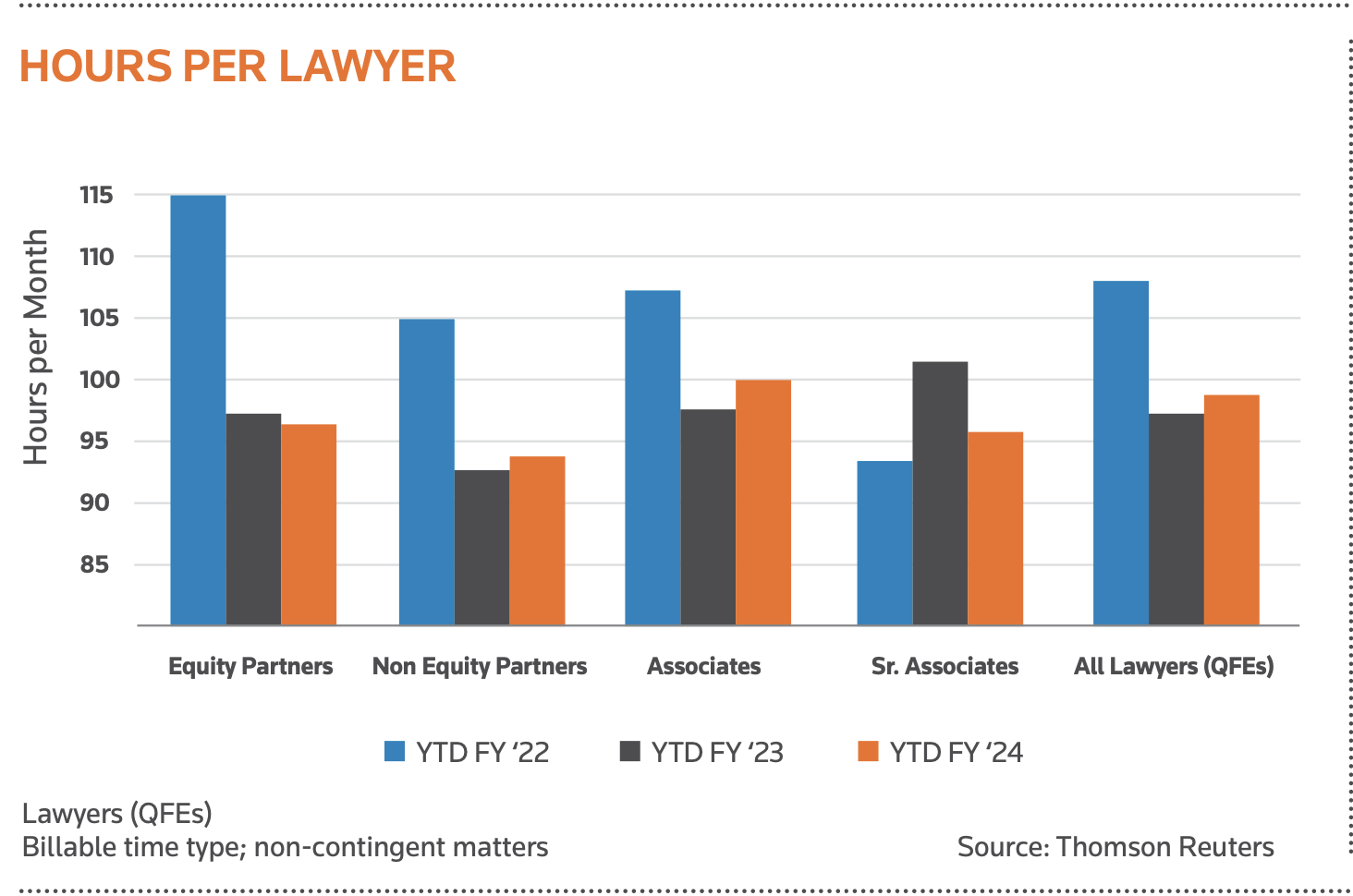

Earlier today, the Thomson Reuters Institute published its Midyear Update on the Australian Legal Market, providing valuable half-year insights into industry trends in the Australian legal market.

There’s a lot to unpack in the Report, and I highly recommend you download it. That said, here are my top takeaways:

✅ What’s Happening with Non-Equity Partners? Is there an underlying story in the Non-Equity Partner segment? The data suggests there might be more to explore.

✅ Equity Partners Carrying the Load? If legal market demand and worked rates are up in 2024, yet the average billable hours per lawyer are down, it raises a big question—are Equity Partners absorbing the extra workload? If so, why?

✅ Billable Hours Decline With 12 months in a year, many law firms have lawyers billing less than 1,500 hours annually. What does this mean for profitability and productivity?

If you’re looking to refine your pricing strategy or need guidance on law firm profitability, feel free to get in touch. In the meantime, download the two-page update and see the data for yourself!

Earlier today (8/4/2024), The University of Sydney Business School and KPMG published their ‘Demystifying Chinese Investment in Australia (April 2024) report‘ (Report) into Chinese investment into Australian businesses. If you are a lawyer with a practice focus on inbound Chinese investment, the Report makes for very sobering reading:

Chinese investment in Australia fell 36 percent to AU$1.34 billion in 2023

This represents the second lowest year in investment value since 2006

Only 11 corporate transactions between the two countries were recorded in this period

The Report covers the period January to December 2023, only relates to corporate (not individuals) and excludes Hong Kong and Macau investment in Australia (i.e. Mainland China only).

Nonetheless, the Report reads bleak – particularly given how many law firm practices here in Australia rely on this type of work to survive.

Any positives?

So, are there any positives in the Report to write home about?

Healthcare was a big winner – accounting 42 percent of the total Chinese investment into Australia – although it should also be said, their accounted for two transactions totaling AU$562 million.

Agribusiness had a big bounce – representing a 21 percent increase in value through to A$283 million. Again though, this was through two deals!

Mining was the big loser with a significant decrease from A$1.8 billion in 2022 to A$34 million in 2023!

Anything else?

With a whopping 82 percent of total investment into Australia, NSW is the home of the largest share of Chinese investment – A$1.01 billion. Victoria accounted for 16 percent followed by WA with a mere 2 percent. Have to wonder what that means for Queensland

As I said at the start, all in all not a great read if you are an Australian lawyer looking for new business out of China. One ray of hope is that investment from privately owned enterprise saw a slight uptick in 2023 – up from A$641 million in 2022 to A$878 million. I suspect a large part of this would have been in property related transactions, because if it wasn’t the Australian-based property lawyers out there with Chinese clients seriously need to think about pivoting their practice!

As always, get in touch if you want to talk through any of the above.

A measure of total billable hours worked by the average law firm

Leaving aside the flaws in that definition, if we are to use it as a yardstick for year-on-year growth and a like-for-like comparison globally, then the Australian legal sector looks positively healthy – particularly so for those practising Dispute Resolution (9.5% growth year-on-year, although I question the low starting bar here as DR has suffered a number of negative years as a result of COVID) and “General” Commercial (7.5% growth year-on-year; and while no definition of “general” is provided it clearly doesn’t include M&A, which sits in a different bucket).

Black clouds? If there is a black cloud around the numbers it’s leverage and expenses.

As the chart above indicates, leverage between partners, senior associates, associates and lawyers still looks out of shape when compared against firms in other jurisdictions.

What this chart indicates to me is that partners (in particular, equity partners) are still doing way too much of the billable work and not pushing the work down to more junior lawyers (which might be understandable if it was salary partners looking to make equity; but kind of suggests it is equity partners looking to retain equity points – maybe a post for another day!).

Having said this, it might also be a trait of the Australian legal market. We often don’t follow the 10-20-30-40 leverage model here in Australia.

A potential second black cloud is on the expense-side: lawyer renumeration.

While this appears to have cooled – down from 13% growth in 2023 to 7.3% growth in the first half of 2024, for those of us who work in this market day-in, day-out, there is an acknowledgement and acceptance that mid-level lawyers (those between 4 and 8 years PQE) are rare as hen’s teeth.

And the reason for that is simple – most see Australia as a small fish bowl and want to spread their wings in Asia, London or New York.

Who could blame them!

Some come back, many don’t.

But what it does mean is this: we pay a premium for mid-level [good] lawyers here in Australia!

The last black cloud has to be lateral partner movement.

The Thomson Reuters midyear market update doesn’t include a section on lateral partner movement, but it should. Not only because it would make for interesting reading, but also because it’s a good indicator figure.

As always, get in touch if you want to talk through any of the above.

A recent article in the Global Legal Post by Ben Edwards: ‘Law firm marketing and business development teams spend more time firefighting than on strategy‘ threw up some very interesting – if not predictable – stats:

Two thirds (65%) of marketing and business development teams [in law firms] are spending more time firefighting then developing strategy

80% of that 65% spend at least 2/3rds of their working year extinguishing fires, over providing strategic thinking

Just over half (57%) have a seat at the head table [when it comes to strategy input]

69% of respondents said they spent most of their time on addressing short-term issues rather than focusing on long-term initiatives.

And the number #1 reason given for why law firm marketing and business development teams were running from one fire to another – a lack of investment in resources.

All of which leads me to ask this question:

Do law firm partners value the service they get from their business development and marketing teams?

Another way of putting that question is this:

Do law firm partners understand the strategic value that their business development and marketing teams can provide?

Because the evidence would suggest that they don’t.

By putting – let’s be frank – high paid personnel on firefighting tasks, your firm will not be getting good value for money.

So here are my 5 reasons why your business development team should be working with you on your firm’s strategy and not just putting fires out:

1. Industry focused

Most business development professionals are laser-focused on industry expertise. They understand a particular industry sector – such as energy, resources, financial services, FMCG, property – and by and large stay in their lanes. As such, many have a deeper understanding of what is happening in that industry sector than the partners they work with.

2. Market knowledge

Really good business developers are on top of market trends and competitor intelligence. They should be able to tell you what your competitors are up to, how your competitors are ranked in the market, which clients your competitors are acting for and the relevant lateral movement in your sector.

3. Relationship Building

A critical skill of good business development professionals is building relationships. They should be able to not only tell you who the General Counsel at client and target clients are, but also who the lead procurement team will be on a pursuit or tender opportunity.

4. Data analysts

A good business developer should be able to look at a set of data and provide you insights. For example: should you be worried if the number of instructions you are receiving is on the decrease, but the value per file is significantly increasing?

5. Results driven

Every good business development professional will tell you they are only as good as their last result! By nature, they are very results driven and don’t rest on their laurels.

So there you go, my 5 reasons why you need your business development team working with you on your next strategy day rather than just putting out fires!

Also, get in touch if you need help with any of the above.

Yesterday (13/11) was World Kindness Day, and while I think that’s a great idea/concept – with the level of mental health issues that we have in the legal profession, you have to ask yourself:

Why doesn’t every law firm office have one of these benches?

Ever wondered if there is a difference between ‘customer service’ and ‘customer experience’?

I was fortunate enough to come across this quote by Paul Roberts, CEO at My Customer Lens that, frankly, sums it up better than anyone else I have seen lately:

“It’s important to define the difference between customer service and customer experience. I like to define customer service as what you do, and customer experience is how you make people feel.”

Too often in professional services firms we concentrate on the ‘customer service’ at the expense of the ‘customer experience’; when the reality is that we should be much more focused on the customer experience than we are on the customer service.

As the article states:

“Improving the client experience is about looking at the entire client journey, from initial enquiry through to case completion, and beyond. It’s a rethink and review of every customer touchpoint throughout your organisation; from the way the phone is answered, to your hold music, reception waiting room and website home page.”

Spot on advice.

If you or your firm is struggling to get a grip with this, feel free to reach out to me for a chat.

Woke up this morning – Australia time – to news that had broken overnight that Eversheds Sutherland (ES) and King Wood Mallesons (KWM) had entered into an exclusive alliance, along with a whole lot of DMs (Direct Messages) in my LinkedIn box asked me what my initial thoughts were.

So here I go with some initial, off the cuff, thoughts about this:

With the closure of the 6 KWM offices across the UK, Europe and Middle East, the deal likely brings to a happy end KWM’s sad foray into those markets and puts final closure on the SJ Berwin story.

Both KWM Australia and KWM Hong Kong are not part of the deal. While this is good news for ES’s Hong Kong team – who I hold in very high regard – it seems very odd and shows possible cracks in the Swiss Verin model that is KWM (with KWM China being party to this arrangement). I’ll be very interested to see what this means for KWM Australia in particular.

The arrangement requires – subject to “client preference and conflict clearance” – KWM China to refer all outbound UK, Europe, Middle East, Africa and South America instructions to ES. I understand the “UK, Europe and Middle East”, but why include “Africa and South America” (noting that ES has offices in Africa but not South America that I can tell)? I think this could be particularly telling given both Africa and South America will be geographies in which KWM Australia plays and so there is the potential to see KWM Australia pitching for work against work that ES has been referred from KWM China.

Noting the deal is with “Eversheds International”, there is no mention of whether the consultancy arm of Eversheds is included in the arrangement. If it is, then KWM China has boosted it offering in this space significantly overnight (although there may well be some regulatory restrictions around that [consultancy] in China).

To me though, what will likely make or break this “formal cooperation agreement” however will be:

How are inbound/outbound referrals being tracked?

How are the referring partners being rewarded for the referrals?

And, what will the KWM Australia partners make of all this given access to a network of lawyers in one of their biggest overseas geographic locations, the UK, will be gone? Do they refer work to ES, even though they are not part of the deal? Or do they refer work to lawyers/mates in other law firms who compete with ES in the UK – including, interestingly US firms with news earlier this week that: “Nearly half of the UK’s largest law firms are US-headquartered”.

I guess we will have to wait and watch this space, but my three big observations are:

(1) Not sure what Eversheds is getting out of this deal – do KWM China refer that much work into UK, EMEA and South America?

(2) Looks to be a great deal for KWM China.

(3) Are KWM Australia being left in the wilderness?

It’s that strange time of the year when we start all over again as if the previous 12 months didn’t happen. Only it is not quite as simple as that. From today:

most lawyers will be charging clients 10% or more extra for their services, with little or no explanation about where the extra value is being delivered and with the new fee rate being completely and totally justified by the date in the calendar and CPI rate increases.

judging by the LinkedIn notifications I have been receiving, a fair number of lawyers will be promoted to new roles – “congrats all”. Along with those promotions comes increased fees charged to clients!

So while we are all enjoying the various EOFY parties over the next few weeks, or simply enjoying some downtime over the school holidays: keep in mind that you need to have a carefully crafted value message to explain to your clients why you justify that higher fee rate; and if you want to ensure that your realisation rate stays healthy I suggest it be better crafted than “we are in a new financial year”.

And if you are struggling with any of that, feel free to reach out to me for a chat.